Weekly Playbook: September 29th

Government Likes It Well Done as Markets Slip, Crypto Retreats, and Jobs Data Set the Stage

Table of Contents

Key Takeaways This Week

Market Overview

Playbook Podcast Spotlight

Earnings & Interesting Movers Recap

Key Index Charts

Earnings to Watch This Week

1. Key Takeaways This Week

S&P 500 and Nasdaq ended slightly lower on the week despite Monday’s record highs, while speculative AI names showed sharper pullbacks.

Crypto retreated even as equities initially rose, adding another sign of risk-off behavior.

The White House is exerting unprecedented influence over private companies with stakes in Lithium Americas, Intel and others

Upcoming government funding deadline, PMIs and jobs data could test investor assumptions about growth and Fed policy.

Last week’s movers: IREN, OPEN, LAC, INTC and KMX

Earnings to watch this week: CCL and NKE

2. Market Overview

The week opened on fumes from the Fed’s rate cut with the S&P 500 up 0.4% to another record on Monday as Apple, Nvidia and Oracle carried the tape, while the Nasdaq also printed new closing highs. That enthusiasm faded midweek but Friday’s inflation gauge met expectations and sparked a rebound. For the week the S&P 500 lost 0.31% and the Nasdaq 0.65%. GDP was revised up to 3.8% for Q2, crypto sold off, and agencies were told to prep for mass firings if a shutdown hits at month end.

Beneath those near record headlines the frothier corners of AI cracked harder. The Magnificent Seven ETF lost about 1% with Amazon, Alphabet and Meta hit hardest. Oklo slumped 18%, Oracle dropped 8% and Micron fell 3%, a hint that some of the “sure things” are getting a valuation check. All of this is playing out against a backdrop where the S&P 500 is up about 12% year to date and 30% since April’s “Liberation Day” low, while the dollar has slid 9% in its biggest drop since 1973. That combination is unusual but not contradictory. A weaker greenback is a tailwind for U.S. multinationals, which earn 40% of revenue abroad, and Morgan Stanley notes a strong link between dollar weakness and upward earnings revisions. Still, Goldman’s survey shows dollar bears outnumber bulls 7:1, the most in a decade, and opinions diverge on whether the trend has much further to run.

The coming week could test some of these assumptions. Government funding expires Tuesday night unless Congress passes a budget or stopgap, risking delays to the jobs report. ISM manufacturing and services PMIs are due midweek and Friday, and September’s payrolls are expected to show only 50,000 jobs added with unemployment steady at 4.3%. Jobs growth has averaged just 26,750 a month over the past four months, a “no hire, no fire” dynamic that Fed governors cite to justify accelerating cuts even as the headline jobless rate stays historically low.

Companies meanwhile are reshuffling under Washington’s thumb and their own ambitions. Tech firms scrambled after the White House said H-1B visas would cost $100,000 each. Trump linked autism to Kenvue’s Tylenol without evidence and announced new tariffs including 100% on drugmakers without U.S. plants. Amazon agreed to pay up to $2.5 billion over Prime subscription charges. Nvidia committed up to $100 billion to OpenAI as it expands U.S. data centers with Oracle and SoftBank from one site to six. Alibaba is ramping AI spending too.

The AI buildout itself is spilling into adjacent industries. Demand from AI customers has blown out wait times for high capacity drives from Seagate and Western Digital to nearly a year. Both companies are raising prices, boosting profits and share prices. Once a low interest deep value play, hard drives are now hot thanks to hyperscaler buildouts. Western Digital and Seagate shares are up more than 300% over the past three years and Benchmark sees more upside, especially for Seagate which already trades at 21× projected earnings and could reach 24× next year’s estimate. BofA estimates $3 trillion of new nuclear spending may be needed through 2050 to supply AI with electricity. That backdrop explains why hedge fund manager David Einhorn warns AI companies are spending too much too quickly and why some investors worry about a “dark fiber” style overbuild. Barclays counters that today’s hyperscalers are funding expansion from cash flow with room for buybacks, unlike the debt fueled dot com era, and usage signs remain strong with AI related job listings rising across sectors and Anthropic’s revenue run rate jumping fivefold to $5 billion.

At the same time Trump has pushed an unprecedented level of direct control over private companies. The Department of Defense bought 15% of rare earth miner MP Materials and a similar stake is being negotiated with Lithium Americas. The government took a 10% stake in Intel shortly after Trump pressured its CEO to resign, and the White House announced Nvidia and AMD would give the U.S. 15% of their revenue from China chip sales, though the deal is not finalized and China banned many chip sales in September. MP Materials shares are up about 157% since news of government involvement, Lithium Americas 123%, Intel about 45%, while Nvidia and AMD have slipped. The White House frames its involvement as protecting domestic capacity and taxpayer upside, not maximizing shareholder returns.

The tape still reflects faith in policy relief and megacap resilience, but with AI darlings wobbling, hard drive makers suddenly in the spotlight, dollar bears crowding in, and Congress lurching toward another shutdown deadline, investors have reasons to look beyond the obvious. Equal weight U.S. ETFs, industrials, healthcare and cheaper international markets all offer ways to diversify. There is more to the market than AI and it may be time to wake up to that fact.

3. Playbook Podcast Spotlight

4. Earnings & Interesting Movers Recap

IREN +8.33% 1W

IREN announced it had doubled its AI Cloud capacity to 23 k GPUs with a $674 million order of NVIDIA B300s, B200s and AMD MI350Xs, aiming for more than $500 million in annualized run-rate revenue by Q1 2026. The surge in pre-contracted demand put the Prince George campus build-out in focus and briefly attracted bullish coverage with a Buy at Arete (target $78), but momentum reversed later in the week as JPMorgan cut it to Underweight (target $24) and Jefferies dropped it to Hold on valuation concerns, sending the stock lower.

The stock ripped through the ATH and 1.5 IPOx but was clearly rejected at 49 (1.75 IPOx) and reversed amid the downgrade-driven bearish tape, closing pennies below 42. That level seems to act as a magnet for now, and whichever side wins there will likely set the direction of the next move.

OPEN -7.94% 1W

Opendoor slid early in the week after AI LiquidRE filed to sell 11.3 million shares and Access Industries confirmed its active stake had dropped to 2.38%, weighing on sentiment around the stock. The mood flipped by mid-week when Jane Street disclosed a 5.9% passive stake after the close, sparking a rebound and putting fresh attention on liquidity dynamics and the potential for re-entries at lower floats.

The stock dipped below the key 7.50 support area, forcing some liquidations that made the trade leaner and potentially reignited momentum. The area was quickly reclaimed with a clean backtest the following session. Reactions to this zone are worth watching if additional backtests occur, along with any potential breakout above the previously mentioned 10.75 key resistance area.

LAC +94.77% 1W

Lithium Americas rocketed after a Reuters report said the Trump administration is seeking up to a 10% equity stake in the company while renegotiating terms of its $2.26 billion Energy Department loan for the Thacker Pass project with GM. The news put lithium names in the spotlight as Washington moves to secure a domestic supply chain and lessen reliance on China. Despite the surge, TD Cowen cut LAC to Hold with a $5 target, highlighting valuation concerns amid the frenzy.

The stock flipped the first key resistance area in the premarket, offering a beautiful backtest right after the open for a potential entry with very limited risk before ripping higher. Follow-through in the next session pushed it slightly above the second key resistance area at 7.25 mentioned on day one, but the stock was eventually rejected there, giving back a good chunk of gains.

INTC +20.01% 1W

Intel jumped after reports surfaced that the company was in talks with Apple for a potential investment to support its turnaround efforts and government-backed expansion, while also approaching other firms for partnerships. The momentum was reinforced by an upgrade to Neutral from Sell at Seaport Research Partners, even as headlines later revealed Intel had also reached out to TSM about a possible manufacturing partnership or investment.

For those who didn’t read last week’s edition, here’s a direct quote on INTC from the same section:

“A close below a key resistance hints at further weakness, though calling a full gap fill is early. Price action around 29 should be watched first, while a reclaim of 30 could set up another leg higher.”

The stock consolidated above the big POC from 2012 near 29 before taking out 30 (1500 IPOx), which ignited a sharp rip higher toward the 34.75 key resistance area and beyond, briefly touching the big weekly TRL at 36.25 before profit taking kicked in. A clear flip could open the way to 40 (2000 IPOx).

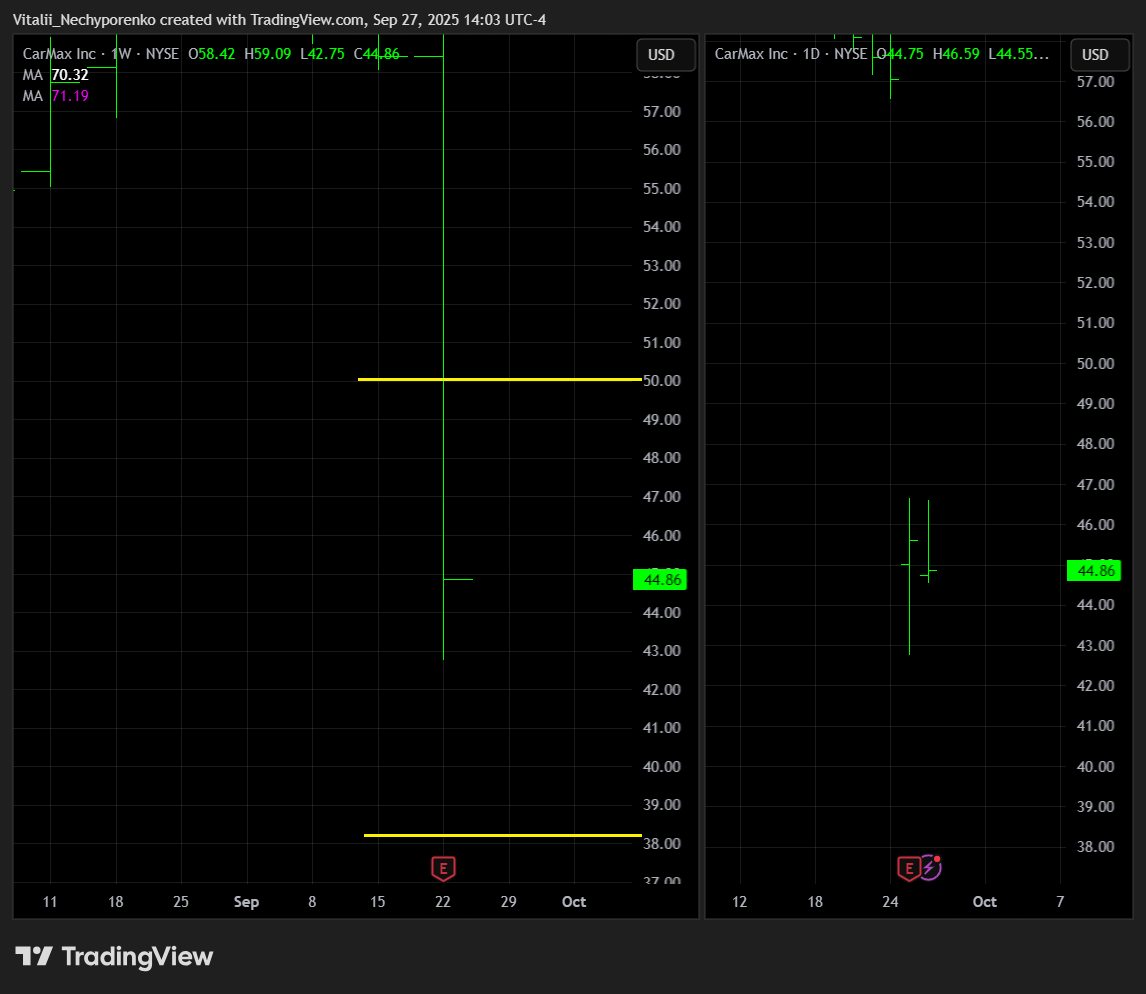

KMX -23.22% 1W

CarMax slumped after a bruising Q2 report showed its widest EPS miss in 11 quarters and a 6% year over year revenue decline to $6.6 billion, its first drop in four quarters and steepest in five. Comp sales fell 6.3% versus +8.1% in Q1, snapping a four quarter growth streak as each month weakened sequentially. Retail and wholesale volumes dropped, credit losses swelled at CarMax Auto Finance, and the tariff driven inventory pull forward from Q1 left the chain with excess stock, heavier depreciation and weaker pricing power. Evercore and Oppenheimer both downgraded the shares, citing a potentially longer than expected strategic reset and a softening demand backdrop.

The stock broke the premarket consolidation at the mentioned 50 key support area, igniting heavy selling amid a rising NYSE opening sell imbalance and eventually opening at 46.10. The second day was rangebound, with the EPS low on watch as a breakdown could lead to a further slide toward the next support area at 38.25.

5. Key Index Charts

The period between quadruple witching and the next earnings season is usually quiet, but this time volatility came back, with broad sectors moving and plenty of action in liquid single names. This may reflect portfolio rebalancing sparked by the recent Fed cut. Now let’s go to the charts:

For those who missed it, I recently published the second options writeup, including the strikes I’m watching this quarter for cash-secured puts I’d be comfortable owning if assigned. Feel free to check it out: