Weekly Playbook: September 22nd

The Fearsome Foursome: Quarter-Point Cut, Quadruple Witching and the Fourth Quarter

Table of Contents

Key Takeaways This Week

Market Overview

Playbook Podcast Spotlight

Earnings & Interesting Movers Recap

Key Index Charts

Earnings to Watch This Week

1. Key Takeaways This Week

Fed delivered a widely expected quarter-point cut to 4.00–4.25% and penciled in two more cuts by year-end

Dollar rebounded, bonds weakened and crypto didn’t spike, challenging the “cut = risk-asset surge” narrative

Nvidia invested $5B in Intel and announced a multi-year PC and data-center partnership, sending INTC up 23%

Quadruple Witching is now behind with record volumes and notable imbalance-driven moves in APP and MSFT

Last week’s movers: TSLA, CRWD, INTC, BLSH

Earnings to watch this week: MU, ACN, COST

2. Market Overview

The Fed finally delivered the widely expected quarter-point cut, lowering the funds rate to 4.00 to 4.25% and penciling in two more cuts by year-end. On the surface that gave the market exactly what it wanted. The S&P 500 gained 1.2% for the week and the Nasdaq 2.2%, all at fresh highs. Even the Russell 2000 joined in with its first record close of 2025. Technology, communication services and consumer discretionary ETFs all hit new peaks alongside the index, a trifecta that historically precedes higher markets. By that measure the rally looks textbook healthy.

Beneath the surface, the picture is less tidy. Powell framed the move as an “insurance policy” against weakening private job growth but the SEP simultaneously raised GDP and core inflation forecasts for next year and cut its unemployment projection. Normally stronger growth, firmer prices and lower joblessness imply tighter policy. Yet the median projection for 2026 shows rates drifting lower. The dots tell the story: one member still wants a hike, six want no more changes, nine see a half point of additional cuts and one wants a full point slash below 3%. That isn’t a roadmap, it’s a barometer of how unsettled the committee is. Powell himself admitted confidence is low. Investors are treating the median as gospel anyway.

The policy backdrop also looks increasingly like “run it hot” with tariff cuts, tax cuts and rate cuts feeding record highs in gold, crypto, stocks and corporate credit. Analysts have compared today’s policy to Greenspan’s 1998 russian crisis easing and even the late 1960s Go Go market, both episodes that inflated asset bubbles before ending badly. The current inverted yield curve has failed only once before to signal recession, in the late 1960s, suggesting today’s inversion may also be a false alarm. Maybe. Or maybe the curve is right and policy is simply cushioning a slowdown long enough for valuations to stretch further.

Nvidia and Intel supplied the week’s headline deal. Nvidia agreed to buy $5 billion of Intel stock and partner on PC and data center chips. The stock’s 23% surge added $28 billion in market value but the deal doesn’t fix Intel’s foundry problem. It still trails Taiwan Semiconductor’s process technology and lacks big outside customers. Jensen Huang praised TSMC’s “magic” even as he stood next to Lip Bu Tan, a reminder that confidence and cash aren’t the same as a manufacturing turnaround.

Geopolitics tried to intrude but the tape shrugged. Trump and Xi spoke by phone and promised to meet again in October. Trump framed the TikTok deal as approved while China called it still under negotiation. Analysts saw a deescalatory tone but few deliverables and warned that secondary sanctions over russia could upset the tentative progress. For now investors are betting on détente rather than disruption.

Even the IPO market is showing its contradictions. Barron’s cover this week proclaims “The IPO Stock Frenzy Is Just Getting Started. Don’t Get Burned” a curious headline given recent deals. Oversubscribed issues still open above their pricing and ring the bell with champagne, but what happens in the next few sessions is often less celebratory. The disconnect between debut euphoria and actual post IPO performance underscores how much of this market is running on momentum and policy hope rather than fundamentals.

All of this leaves a market leaning hard on policy relief and megacap resilience. That can carry it higher for a while. But with jobs data still soft, valuations stretched, Intel’s bounce built on faith more than fundamentals and a bubbly IPO tone creeping back in, the dot plot’s dispersion may be the real tell, not a guide to where rates are going but a snapshot of how confused policymakers are even for the next few meetings.

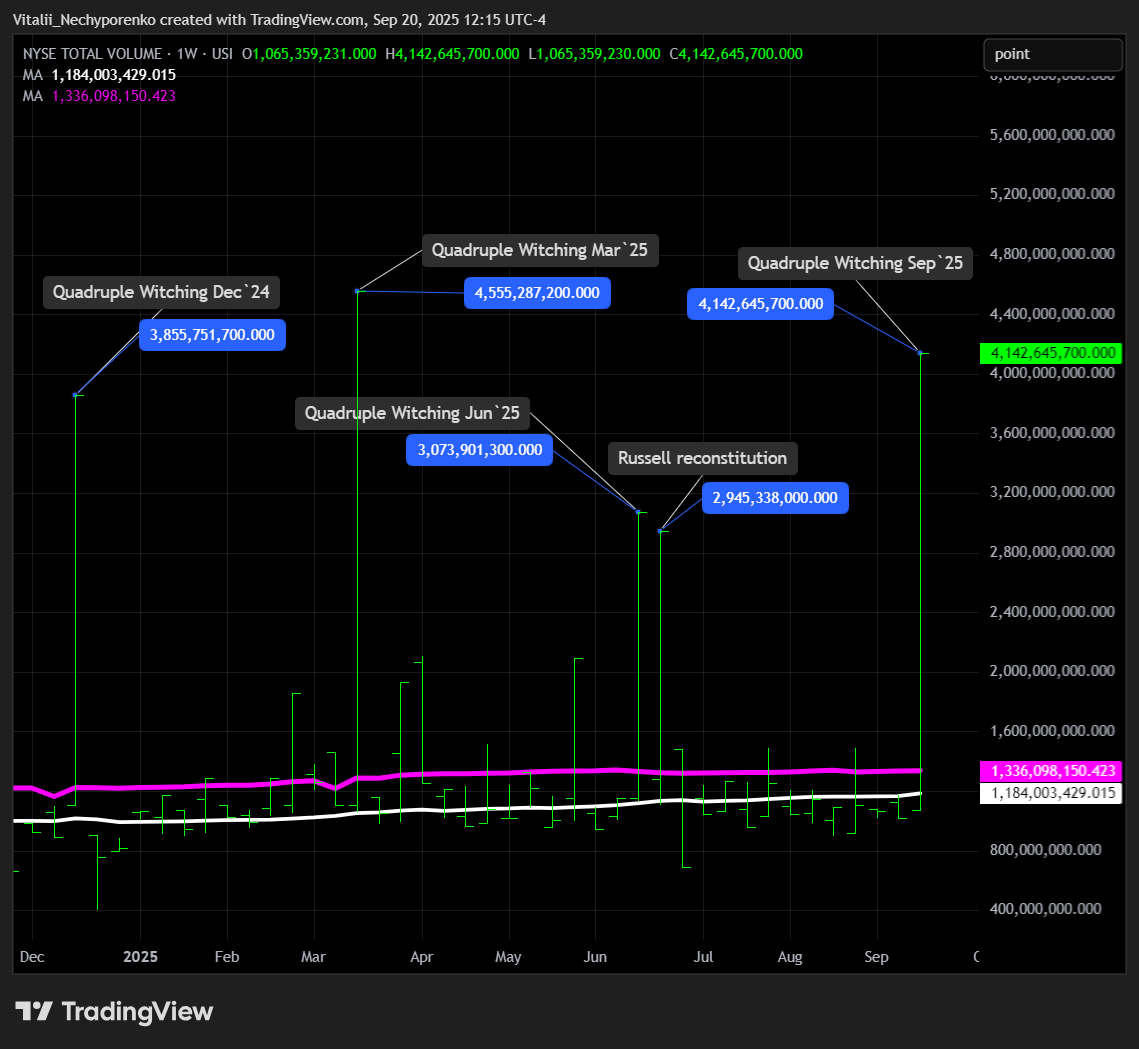

Long-awaited Quadruple Witching is now behind us with record volumes on the tape. The NYSE total volume chart below gives a sense of the scale.

Despite the huge notional value of closing imbalances, most were paired and there weren’t many situations worth detailed coverage like the Russell Reconstitution in June and SNPS–ANSS merger closing in July. That’s why I’m postponing the third part of Unraveling the Close focused on Quadruple Witching. I’ll combine examples from this auction with December’s and, hopefully, there will be more textbook setups. For anyone who missed them, here are the links to the first two pieces in the series.

Here’s also a quick look at APP, which was added to the S&P 500, and MSFT, which posted a large imbalance in notional terms that produced a clean rip into the close and some decent trading opportunities:

3. Playbook Podcast Spotlight

I’ve decided to make the writeup leaner. From now on there will be a Playbook Podcast Spotlight subsection where I’ll post a link to the most interesting piece I’ve listened to and recommend checking out.

4. Earnings & Interesting Movers Recap

TSLA +7.61% 1W

Elon Musk’s first direct stock buy since 2020, nearly $1 billion of TSLA shares, landed just as Tesla’s core EV business is wobbling under slumping deliveries, margin compression from price cuts and a looming phase-out of the U.S. $7,500 EV tax credit at the end of September. The timing has been read as a vote of confidence but also underscores the pivot Musk is trying to sell investors on, a future defined less by cars and more by robotaxis, humanoid robotics and AI platforms. That vision is ambitious but still speculative and it sits alongside a controversial $1 trillion CEO pay package tied to aggressive performance targets, a reminder of how much the Tesla story hinges on Musk himself.

The stock initially reacted sharply off the 425 key resistance area (375 ipoX with converging weekly trendlines and measured move targets), dropping quickly at the open as profit taking accelerated through the day. After a few more attempts the following sessions it closed just above 425, but it needs a clear move away from that level to confirm a flip, which if achieved could open a path to the 453 area (400 ipoX).

CRWD +15.24% 1W

CrowdStrike surged after BMO Capital raised its target to $500, citing stronger ARR guidance and broad customer enthusiasm. At its Fal.Con 2025 event the company announced deep partnerships with AWS, Intel, Meta, Nvidia and Salesforce to embed Falcon protection across the AI stack, positioning it as a potential standard for AI security. It also agreed to buy Pangea for $260 million to strengthen defenses against prompt-injection attacks and unveiled new data protection and identity security features to guard GenAI data leaks and hybrid identities. The stock traded near $495 after the news.

The stock ripped through the 471–476 key resistance area (weekly trendline and 14 ipoX) and nearly reached the 510 level flagged as the next target on the gap day. A clear break above 510 could set up a run at the ATH, with the next resistance in 544-548 area.

INTC +22.84% 1W

Intel shares jumped after Nvidia committed a $5 billion investment and a multi-year partnership to co-develop custom data-center and PC products. Intel will manufacture Nvidia-custom x86 CPUs with integrated RTX GPU chiplets for next-gen AI PCs and supply CPUs for Nvidia’s AI infrastructure platforms, giving Nvidia more architectural control and diversifying supply beyond TSMC. The deal validates Intel’s struggling foundry business, de-risks part of its heavy capex plan and could spark a multi-quarter re-rating in its valuation. For Nvidia the benefits are incremental but strategic, tightening its grip on the AI stack and pressuring AMD and Qualcomm in both servers and client PCs.

The stock traded premarket above the big resistance near 30 (1.5k ipoX and weekly TRL on top of the big POC since 2012 near 29) with the next level at 34.75, but it never got there as profit taking started ahead of 9:25 a.m. when a $100M NSDQ opening imbalance hit and pushed it lower with clean follow-through after the open, a classic OPG setup on that kind of gap. Bulls tried to push it back up during the day but it never reclaimed the premarket highs and closed near the lows, adding another follow-through on Friday. A close below a key resistance hints at further weakness, though calling a full gap fill is early. Price action around 29 should be watched first, while a reclaim of 30 could set up another leg higher.

BLSH+33.45% 1W

Bullish posted its first earnings as a public company with Q2 adjusted revenue of $57M, adjusted EBITDA of $8.1M and net income of $108M on $58.6B of digital-asset sales, while winning the New York DFS BitLicense alongside MiCA and Hong Kong SFC approvals. Subscriptions and services revenue jumped 61% to $32.9M on cross-sell wins and CoinDesk Indices AUM rose to $41B. Management guided for Q3 adjusted revenue of $69–76M and adjusted EBITDA of $25–28M as its options platform moves toward full launch and U.S. activity ramps, giving Bullish a rare mix of regulatory clarity and diversification among digital-asset venues.

The stock flipped the key POC at 59.25 mentioned earlier despite initial choppy tape and a wave of OPG sell limits that kept it from opening above 60. The fresh 21-day MA acted as dynamic support intraday and the POC was backtested cleanly around noon before buyers took full control, closing slightly above 64.75 (1.75 ipoX). Friday showed solid follow-through as 64.75 held and gains extended into the close, flipping the IPO low. If it can hold here, we might start reading its ticker as “bullish” instead of “bullshit” again.

5. Key Index Charts

It was another strong week for the stock market, though the rebound in the dollar and weakness in bonds was probably not the reaction many expected after the long-awaited rate cut. Plenty of posts predicted crypto would rip higher as soon as the Fed cut, but most of those are likely deleted now given the mixed response. Anyway, let’s get to the charts: