Weekly Playbook: October 6th

Buy Now, Ask Later: How the Government Shutdown Is Affecting Markets and Crypto

Missed our Oracle deep dive? Catch it here:

Table of Contents

Key Takeaways This Week

Market Overview

Playbook Podcast Spotlight

Earnings & Interesting Movers Recap

Key Index Charts

Earnings to Watch This Week

1. Key Takeaways This Week

Markets set record highs despite the shutdown

Crypto flipped the tape: BTC near ATH after clearing 118k POC, ETH testing 4500

Healthcare rotation led and widened breadth

How FRMI IPO pleased day traders and RKT closing auction drama

Last week’s movers: CRCL, LAC, ASTS, FICO and MU

Earnings to watch this week: STZ, DAL and PEP

2. Market Overview

The tape brushed off the shutdown like a minor scheduling inconvenience. The S&P 500 notched another record while the Nasdaq printed its 30th of the year, capping weekly gains just over 1%. Gold rallied, the dollar slipped, and the ADP report showing 32,000 private jobs lost in September replaced the BLS release that never came. Some of that resilience may have come from hedges being unwound once it was clear the BLS wouldn’t release data, removing headline risk. The irony is that investors didn’t blink. If anything, the lack of official data left equities free to drift higher into earnings season.

Still, the shutdown is not without consequence. With the BLS, BEA, and Census all dark, policymakers are flying blind just weeks before the next FOMC. The futures market is already pricing a near certainty of another quarter-point cut, but without labor and inflation prints the Fed is left parsing noisy private data. ADP, Revelio, Challenger, and the Chicago Fed’s real time jobless estimates all told different stories last week. For now, the consensus is that labor is softening, but if the blackout stretches into November and December the policy calculus gets trickier. Investors should remember the Fed is not as data independent as the market narrative pretends.

Against that backdrop, the market found its rotation story in an unlikely place: healthcare. The sector ETF surged nearly 7% for its best week since 2022, a sharp reversal after being the year’s laggard. Pfizer struck a deal with the White House to cut Medicaid prices, sell discounted treatments on a government portal, and align U.S. pricing with peers abroad in exchange for tariff relief. The terms looked much less draconian than feared, analysts called it a win, and the tape followed. Other drugmakers are expected to get similar deals, which reframed the entire sector from political punching bag to potential safe harbor.

That rally matters for more than just pharma. For most of the year the market’s leadership has been unnervingly narrow, riding AI and a handful of megacaps. Healthcare’s breakout is a reminder that rotation is possible, and breadth is a stabilizer if AI hype ever wobbles. Tech headlines still carried the Nasdaq higher, but the week belonged to defensive sectors, not semis. Equal weight indices, utilities, and industrials also caught a bid, hinting that investors are at least testing alternatives to the AI trade.

Meanwhile the capital markets themselves are in overdrive. The $55 billion LBO of Electronic Arts by Saudi investors and Affinity Partners is the largest ever in gaming and another data point in Evercore’s thesis that dealmaking is accelerating alongside the bull market. Berkshire’s $9.7 billion purchase of OxyChem, BlackRock’s twin infrastructure deals, and the government’s growing list of forced equity stakes all point in the same direction: money is moving fast, with little fear of policy or financing costs.

The picture is one of surface strength, but with caveats. The shutdown has muted official data flow and the Fed is on track to cut again without clarity. Pharma’s rally is welcome but depends on the White House’s shifting political calculus. And the exuberance in capital markets looks increasingly detached from labor trends and fiscal realities, with Treasury buyers demanding more yield and U.S. interest costs already running at $933 billion annually.

For now, the market is content with record highs and sector rotation. But when both government data and political guardrails are missing, complacency is not a strategy.

The IPO market finally delivered: FRMI, a listing that pleased not just the lucky pre-IPO buyers who got allocation but day traders as well. It priced at $21 per share for a $13.8B market cap. Structured as a REIT with a dual listing on Nasdaq and the London Stock Exchange, it raised 682.5M. The pitch is simple: a Texas Panhandle campus to power AI data centers, with natural gas now and nuclear later. Early positives include secured turbines and a long-term tenant LOI, but there’s no revenue yet and dividends are years away, so execution and funding risk remain high. Let’s take a closer look:

CORRECTION: 1.5 IPOx in FRMI is actually 31.50, not 30.50. That’s what happens when you trust your memory instead of the calculator you used to ace math with back in the day.

The initial consolidation above both the 1.25 IPOx and POC led to a breakout through the first IPO high, which naturally turned reactive the following session, and a strong rip into the close. Some of the move may have been fueled by a closing imbalance, though it wasn’t significant. Still, once highs are taken out, the lack of sellers into the close can add momentum. Day two offered little follow through, with FRMI rejected at 36.75 (1.75 IPOx) despite a couple of premarket attempts to hold above. The current consolidation still looks healthy, with FRMI holding above its IPO lows, already a win compared to recent listings. A reclaim of the IPO high could open the door for another test of 36.75, hopefully with more success this time.

This week offered an interesting closing auction example: RKT. Since it raised a lot of questions and caught plenty of attention, I figured it’s worth shedding some light on the process. I won’t go deep into the details, but here’s what stands out:

There was a significant NYSE floor imbalance on Wednesday, around 25 million shares. Since this data is visible to floor brokers before being released to the public, it’s likely that some participants were frontrunning the publication by opening long positions.

At 15:50, NYSE posted the imbalance to the public, triggering heavy buying due to the large notional value and the fact it exceeded the stock’s average daily volume. There was also a clear catalyst: RKT had just completed its $14.2 billion acquisition of Mr. Cooper Group (formerly COOP). These events usually trigger forced rebalancing from merger arbitrage funds as they unwind positions and adjust hedges.

At the time, RKT was trading at 19.80 and quickly spiked to 20.20, a 2% move.

At 15:55, the key update showed that most of the imbalance had vanished, though the size didn’t increase, which is often a red flag. Still, the stock pushed above 20.50 with strong buying, adding another 1.5%.

The surprise came near the actual close when NYSE posted a revised imbalance of negative 4.4 million shares, flipping the picture. Some of the reversal was driven by active speculators trying to capture the spread between the current price and the expected NYSE clearing price, which was near 21. The final print came at 19.58, almost 4.5% lower than the 20.50 pre reversal high.

The late timing added fuel to the fire. According to NYSE rules, even D orders can be submitted, modified, or canceled up to 3:59:50. That meant anyone who sent this type of MOC closing order had no choice but to accept the closing price and walk away with a lesson. Quick reminder: regular MOC orders cannot be canceled or modified regardless.

For those who are interested in closing auctions here are 2 pieces that I wrote dedicated to specific liquidity events:

3. Playbook Podcast Spotlight

4. Earnings & Interesting Movers Recap

CRCL +14.80% 1W

Circle Internet gained traction as crypto reversed sharply higher, with sentiment boosted by the government shutdown narrative that framed digital assets as relative winners. The stock was also in focus after initiations at Citizens JMP (Market Perform) and Rothschild & Co Redburn (Neutral, target $136). Momentum picked up midweek when Circle announced a first of its kind MoU with Deutsche Börse to explore integrating its EURC and USDC stablecoins into European market infrastructure, highlighting a potential regulatory foothold for stablecoin adoption across the region.

As mentioned on Monday, CRCL delivered a textbook daily DTL breakout with a clean virgin mid backtest off 124 (4 IPOx). After a brief consolidation and another backtest, it ripped higher before getting rejected at 155 (5 IPOx) and the daily TRL. A solid example of how price tends to respect those extensions.

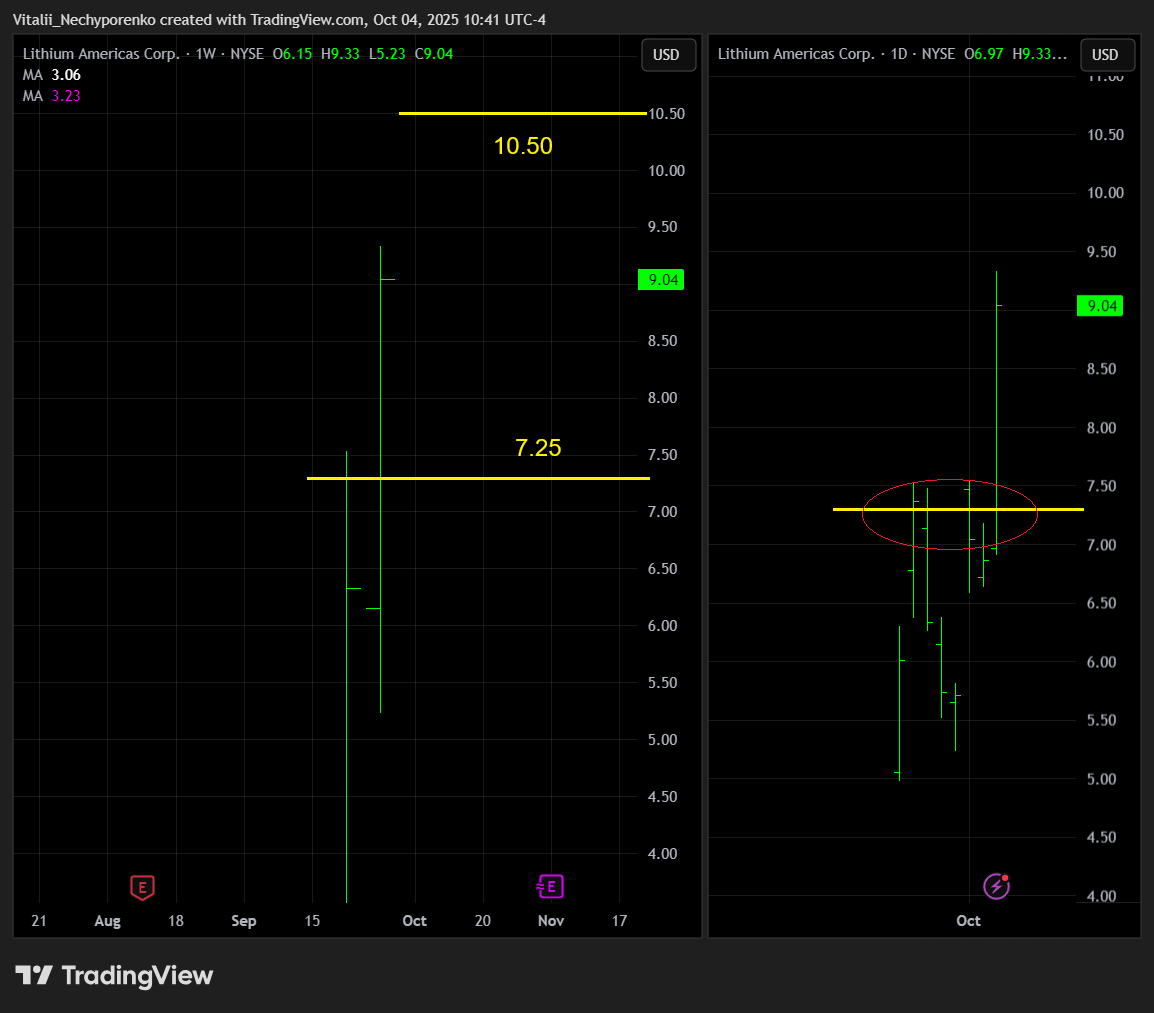

LAC +42.81% 1W

Lithium Americas stayed in focus after announcing a non-binding agreement with GM and the Department of Energy to advance the first $435 million draw on its $2.26 billion DOE loan for the Thacker Pass project. Terms include a deferral of $182 million in debt service over the first five years and warrants granting the DOE a 5% equity stake in the company and a 5% economic stake in the JV. GM also amended its offtake agreement to allow third-party deals on unallocated volumes, broadening potential demand sources. Even as the stock ripped on the headlines, Canaccord Genuity cut it to Sell from Speculative Buy, citing valuation risks.

The stock was clearly rejected on the gap day at the mentioned 7.25 key resistance area that had already proven reactive the week before. After a brief consolidation it flipped the level, triggering a powerful rip higher. The next resistance to watch is 10.50.

ASTS +38.03% 1W

AST SpaceMobile rallied after announcing its BlueBird 6 satellite had completed final assembly and is scheduled for shipment to India by October 12, with BlueBird 7 to follow later this month and satellites 8 through 16 in production. The company reiterated plans to deploy 45–60 satellites by the end of 2026, positioning itself to deliver global mobile broadband rather than just text services like Starlink. Excitement was further boosted when ASTS and BCE completed Canada’s first successful space based direct to cell VoLTE call, video call, broadband data session and streaming test, marking a milestone in bringing commercial-grade connectivity to standard smartphones.

The stock initially reacted to the mentioned 55 key resistance area with a slight frontrun but eventually flipped it and never looked back. That level could still be reactive on a backtest, while the next resistance sits near 75 where an MM target and 7.5 IPOx (or call it spacX) converge.

FICO +21.85% 1W

Fair Isaac surged after unveiling a new direct license program for mortgage lenders, designed to cut out middlemen and lower per-score fees by up to 50%. The move drew immediate praise from FHFA Director Bill Pulte, who said he had productive talks with FICO’s CEO and framed the initiative as a first step toward a more competitive and consumer-friendly market. The headlines positioned FICO as responsive to regulatory pressure at a time when credit bureaus face scrutiny over pricing, though rivals like TransUnion pushed back, criticizing FICO for doubling costs elsewhere and adding new penalty fees that could hit homebuyers.

The stock cleared both mentioned resistance levels at 1800 (225 IPOx) and 1860 (latest POC), though it closed the week slightly below the former. The 200d moving average provided minor support, despite being undercut during the volatile day one open. A consolidation here and a sustained flip of 1860 could open the path toward 2000 (250 IPOx), which was almost tagged on day one, and potentially higher given prior sentiment and underexposure after a stretch of underperformance.

MU +19.43% 1W

Micron rode positive sentiment after Samsung announced a sweeping strategic partnership with OpenAI covering semiconductors, data centers, shipbuilding, cloud services, and maritime technologies. The deal positioned Samsung as a central player in the next wave of AI infrastructure buildout, pulling peers like Micron into focus as investors looked for secondary beneficiaries. The headlines reinforced the bullish narrative around memory demand and AI-driven capacity expansion that has underpinned Micron’s recent strength.

The stock is up 51% on a rolling 30 day basis and the price action has all the signs of a gamma squeeze. Add peers into the mix SNDK +105%, WDC +45%, STX +37% and the picture gets even more interesting. I don’t want to spoil the party, but we all know how these runs usually end, at least for short term momentum chasers. MU was rejected around the 189 key resistance area (MM target stacked with the weekly TRL and 135 IPOx), though part of that rejection was tied to broad market weakness Friday afternoon. Despite the initial drop, the stock briefly reclaimed and held the area before trapping fresh longs and forcing a flush toward the lows, then bouncing back. With the weekly TRL shifting and 196 now on watch and a bigger resistance standing at 210, fading the rip with calculated risk still looks like the best option.

5. Key Index Charts

In this section I highlight only the most important zones with brief comments. I use fully layered charts to identify them, but keep the charts here clean for clarity.

It was a strong week for markets despite broadly negative headlines. By common sense, shutdown risks and the postponement of key macro releases like nonfarm payrolls and unemployment should have dragged indexes lower or even triggered sharp selling. Instead, markets shrugged it off and all three indexes pushed to fresh all-time highs before Friday’s profit taking and afternoon retrace. If that’s the case, this rally could prove short-lived. Now, let’s get to the charts: