Weekly Playbook: October 20th

Earnings season shifting gears as megacaps line up. Gotta Catch ’Em All? Watch out for the cockroaches

Table of Contents

Key Takeaways This Week

Market Overview

Playbook Podcast Spotlight

Earnings & Interesting Movers Recap

Key Index Charts

Earnings to Watch This Week

1. Key Takeaways This Week

Dimon’s “cockroach” warning turned real after Zions and Western Alliance revealed fraud-related losses

Private credit and crypto are creeping into 401(k)s, raising concern over risk seeping into retail portfolios

The next CPI report on October 24 is expected at 3.1%, the last key input before the Fed meeting

Earnings season is starting to shift into higher gear

Last week’s movers: AVGO, BE, AMD and MU

Earnings to watch this week: NFLX, GEV, VRT, TSLA, LRCX, IBM, and INTC

2. Market Overview

Quick housekeeping note: the next Weekly Playbook will be slightly delayed due to short vacation. I’ll be away for the weekend but will aim to have it ready by Sunday night or Monday noon at the latest. To make up for the delay, we’ll also publish the first article in the Crypto Playbook series around that time. Stay tuned.

The week opened on an upbeat note as hopes for a thaw in U.S.-China relations lifted sentiment and helped push major indexes to fresh gains. The optimism didn’t last. By midweek, credit anxiety took over the narrative after Jamie Dimon’s “cockroach” warning turned from metaphor to market driver. His remarks, delivered after the failures of Tricolor Holdings and First Brands, quickly proved prescient as Zions Bancorp and Western Alliance disclosed fresh fraud related losses. The timing was impeccable, and the message hit harder than any macro headline: when lending looks too quiet, it probably isn’t.

The episode exposed what markets have chosen to ignore, the quiet build up of opaque credit risk beneath the bull market. Nonfinancial depository institution loans, the kind extended to hedge funds and private borrowers, now make up roughly a third of all commercial and industrial lending at large U.S. banks. These are leverage loops, not credit innovations, and nobody outside the system really knows how they would behave under stress. Investors brushed off the first cracks, but the fear wasn’t about size, it was about structure.

Ironically, this came in the middle of one of the strongest earnings weeks for the major banks in years. Credit quality remains solid, consumers are still spending, and trading revenue is booming. Yet a handful of fraud headlines did more to move sentiment than billions in profits. The issue wasn’t capital adequacy, it was confidence. The long run of easy policy blurred the lines between private credit, structured leverage, and retail access, and once trust wobbles, exposure maps faster than liquidity models can handle.

That blurring now extends into places it was never meant to reach. Both private credit and crypto have already found a path into 401(k) plans through a handful of providers, most notably after the Department of Labor allowed limited allocations under fiduciary discretion. It is a striking development considering the volatility of one and the opacity of the other. The combination of illiquid credit, digital assets, and passive retirement money is the kind of experiment that usually looks fine until it doesn’t. Crypto’s rebound will only embolden that trend, but it adds another layer of fragility just as leverage is being questioned again.

Meanwhile, the Fed continues to operate half blind. The government shutdown has frozen key data releases, leaving policymakers to infer from anecdotes and incomplete private surveys. Another quarter point cut looks likely, less as stimulus and more as insurance. The irony is that the data blackout may be the only thing keeping the market calm, nobody can panic about numbers they can’t see. The next inflation reading, due October 24, is expected to show headline CPI up 3.1 percent year over year, with core holding steady at the same rate. It will likely be the only major datapoint before the next Fed meeting and could shape the tone for the rest of the quarter. Fiscal deficits above five percent of GDP and record gold prices, however, suggest that some investors are already hedging against the quiet debasement that comes with permanent easy money.

AI remains the narrative glue holding the bull case together. Broadcom’s deal with OpenAI for ten gigawatts of compute reinforced the illusion of infinite capital and power availability. But the same financing chains, vendor credit, private debt, and structured equity that fund the AI build out sit at the heart of the credit story Dimon warned about. If that liquidity tightens, the entire ecosystem gets tested, not just the hype.

By Friday, the indexes had recovered, volatility barely moved, and the tape ended higher as if none of it mattered. But something shifted. The market was reminded that strength and stability are not the same thing. The bull trend is alive, but the illusion of safety cracked. For now, the cockroach is still alone, but everyone’s watching the floor.

Earnings season is starting to shift into higher gear, and while the old “Gotta Catch ’Em All” mindset might have worked in childhood cartoons, it definitely doesn’t apply to trading or investing. I’ll focus on the most interesting and actionable names in the Earnings to Watch This Week section, with the rest covered in the morning notes.

3. Playbook Podcast Spotlight

4. Earnings & Interesting Movers Recap

AVGO +7.61% 1W

Broadcom surged after announcing a multi-year collaboration with OpenAI to co-develop custom AI accelerators and Ethernet-based network systems supporting up to 10 gigawatts of compute capacity. OpenAI will design the chips and system architecture, while Broadcom will handle development, manufacturing, and deployment across OpenAI’s facilities and partner data centers between 2026 and 2029. The partnership gives Broadcom a direct foothold in hyperscale AI infrastructure and expands its custom silicon pipeline beyond networking into full-stack AI systems. Executives highlighted expected engineering productivity gains of 10–20% and reinforced that the company’s supply chain remains insulated from rare earth dependencies.

The stock gapped into the key resistance area on Monday morning, where two major weekly TRLs converge with the 240 IPOx. The reaction was immediate, triggering heavy profit taking right at the open. Bulls made a few more attempts in the following sessions, but the area proved highly attractive to sellers, leading to a broader retracement. It’s worth watching closely, as a confirmed flip of this zone could spark strong momentum toward the all time highs.

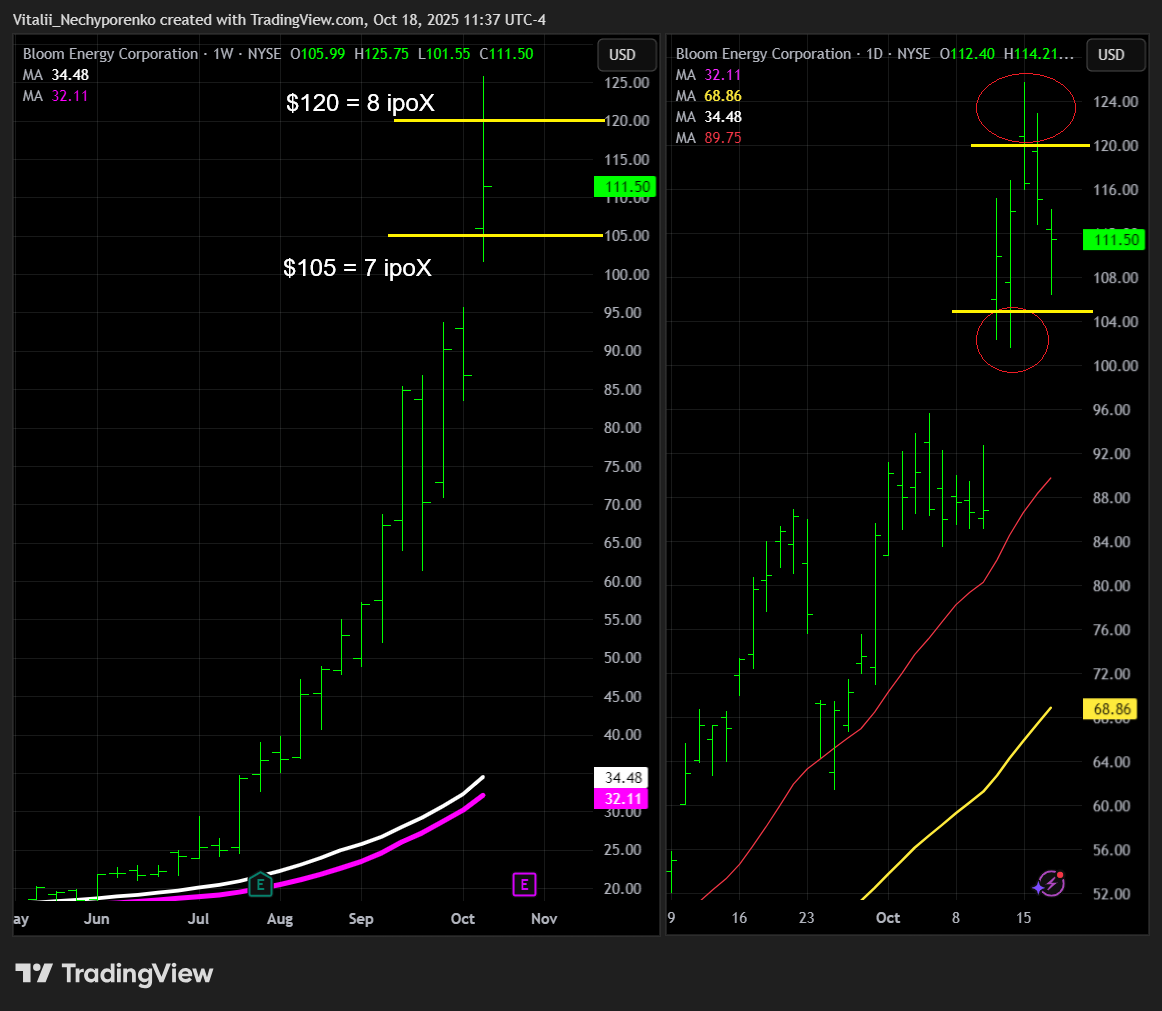

BE +28.35% 1W

Brookfield Asset Management and Bloom Energy announced a $5 billion strategic partnership aimed at building next-generation AI factories capable of meeting surging compute and power demands from artificial intelligence infrastructure. Brookfield will invest up to $5 billion to deploy Bloom’s advanced fuel cell systems, with the first sites already in development and a European location set to be announced before year-end. The collaboration positions Bloom as a key supplier of clean, distributed power for hyperscale AI facilities, while aligning Brookfield with one of the fastest-growing segments in the global energy transition. With U.S. AI data center power needs projected to exceed 100 gigawatts by 2035, the deal highlights the accelerating convergence of digital infrastructure and sustainable energy solutions.

The mentioned 120 area (8 IPOx) was clearly frontrun during Monday’s premarket, though buyers stepped in at 105 (7 IPOx), defining a short-term trading range. After a failed attempt to break below 105 on Tuesday, bulls tried to push through 120, but momentum faded as sellers stepped in and the stock closed mid-range. The next leg’s direction will depend on who blinks first.

AMD +8.46% 1W

Advanced Micro Devices gained momentum after ASML’s Q3 results signaled improving visibility and sustained AI driven demand across the semiconductor supply chain. ASML’s strong €5.4 billion in bookings, with balanced contributions from logic and memory, reinforced expectations of ongoing investment in advanced DRAM and high bandwidth memory nodes, key end markets for AMD’s data center and AI product lines. The reaffirmed FY25 growth outlook and improved EUV adoption trends pointed to a steadier foundry environment heading into 2026, supporting sentiment around AMD’s positioning as a primary GPU and compute alternative in the expanding AI infrastructure cycle.

The breakout above the initial gap high quickly lifted the stock toward its all time high, but it failed to hold there, which isn’t surprising given the nearby weekly TRL and 62.5 IPOx that both need to be flipped for further upside. If successful, the next reactive resistance area to watch is around 252. The stock needs to hold above 213 for the bullish narrative to remain intact from a technical standpoint.

MU +11.44% 1W

Micron rallied after UBS raised its target to $245, citing robust DRAM demand, tightening supply, and strong earnings potential into 2026. UBS noted worsening supply shortages across both legacy DDR and HBM segments, with hyperscalers pursuing multi-year supply agreements that bundle DRAM and NAND products. The firm now sees Micron’s 2026 EPS approaching $30, supported by a structural shift in demand from AI infrastructure and smartphone recovery. Separately, Micron confirmed plans to exit the China server chip market amid regulatory pressure, while continuing sales to automotive and mobile customers. The move highlights a strategic pivot toward high-margin AI memory products, reinforcing Micron’s positioning at the center of the accelerating HBM and DRAM cycle.

The previously mentioned resistance area, which offered a couple of solid fading opportunities, was clearly flipped with not one but two clean backtests and no deep undercuts, a great setup for active traders. The 210 area remains on watch for a potential downside reaction given the layered structure, the big round 150 IPOx and the nature of the recent move. However, if it also gets flipped and confirmed, the stock could easily rip higher from these levels.

5. Key Index Charts

In this section I highlight only the most important zones with brief comments. I use fully layered charts to identify them, but keep the charts here clean for clarity.

Well, the bid was found. However, a major head and shoulders pattern is forming across the main indexes, and you can sense volatility picking up without even checking the VIX, just look at the size of the recent bars, regardless of direction. Whether the right shoulder fails and drives a move to new highs, or we’re setting up for a “big and beautiful” drop, remains an open question. Some megacaps reporting this week might help provide the answer. Now, let’s go to the charts: