Weekly Playbook: October 13th

Who came through with two Glocks to penalize your longs?

I like happy things, I’m really calm and peaceful

I like birds, bees, I like people

I like funny things that make me happy and gleeful

Like when I impose 100% tariffs on China!

Donald Slim Trady

Table of Contents

Key Takeaways This Week

Market Overview

Playbook Podcast Spotlight

Earnings & Interesting Movers Recap

Key Index Charts

Earnings to Watch This Week

1. Key Takeaways This Week

China tariff shock broke the complacent streak, sparking the sharpest selloff since April and reminding how one headline can unwind an extended tape.

Market tone stays frothy with volatility muted; record retail exposure raises the risk of forced selling if weakness deepens.

Banks are officially kicking off the Earnings season this week

Last week’s movers: AMD, MU, GLD and IREN

Earnings to watch this week: C, GS, JNJ, JPM, ASML, BAC, TSM and AXP

2. Market Overview

The tape finally met a real headline and it was not on anyone’s screen. Trump didn’t get the Nobel Peace Prize, though he still managed to headline the week by threatening new tariffs on China just as the AI party was warming up again. The move caught positioning leaning one way. After a clean Monday pop on the AMD and OpenAI partnership, Friday turned into a risk reset with the S&P posting its worst day since April and cyclicals taking the brunt. Utilities finished green on the week, a small tell that money is testing defensives while the growth trade digests policy shock. Even so, volatility barely woke up. VIX remains historically low despite a two and a half percent weekly drawdown in the Nasdaq, which says complacency still runs the show.

The AMD and OpenAI tie up keeps the AI narrative front and center, but it also underlines the same circular financing the street has been debating all quarter. Equity for compute. Vendor credit for cloud. Multi year purchase commitments that depend on funding yet to be raised. The excitement is real and so are the orders, but the market is increasingly pricing outcomes that assume capital is infinite and power is abundant. If either assumption wobbles, the ripple will not stop at semis. It will hit the cloud complex, the power buildout, and any name whose multiple is now chained to AI capacity rather than cash flow.

Macro did not help the mood. The shutdown continues to black out official data just as earnings season begins, which forces investors to lean on noisy private series and management commentary. The Fed is widely expected to cut again, but without clean labor and inflation prints the communication challenge gets harder. That mix can produce sharp tape reactions to single headlines, and Friday was a preview. Add the tariff overhang and you have a market that is still priced for perfection while policy risk is rising.

Breadth offered a small counterweight. Utilities outperformed, health care losses were modest relative to cyclicals, and equal weight indices held better than the megacap complex. It is not rotation so much as a toe in the water away from the consensus AI pile, which is what you would expect after three years of a bull run and an eighty five percent move off the 2022 lows. Valuation does not stop a trend on its own, but with the S&P near twenty two times forward earnings, the multiple now depends on cuts arriving on schedule and estimates holding up. Conference calls next week will matter, especially any color on tariff exposure, supply chains, and margin sensitivity to a stronger dollar if safe haven flows persist.

Net net, the market still shows strength on the surface but the foundation looks thin. The tone is bubbly, volatility is asleep, and the AI trade now depends more on financial engineering and power math than on innovation itself. Record highs remain possible and the bull trend is intact, yet with policy uncertainty rising, a data blackout still in place, and record retail exposure in the mix, a deeper selloff could easily force capitulation. Banks can sit on billions in unrealized losses for years, but most investors cannot.

3. Playbook Podcast Spotlight

4. Earnings & Interesting Movers Recap

I won’t go over Friday’s surprise here and will instead focus on setups that were clearly telegraphed and had enough context to justify trading decisions. Still, it’s essential to watch where futures open on Sunday and how we trade in Monday’s premarket. If this turns out to be just the start of the ride, I suggest reading this and being prepared. Personally, I’ll be writing CSPs while slightly adjusting the targeted APY, as the premiums are attractive in names I’m comfortable getting assigned. The full list of CSPs I’m watching this quarter is included.

AMD +30.50% 1W

AMD rallied after announcing a landmark AI infrastructure partnership with OpenAI. The agreement covers a 6-gigawatt buildout of data-center capacity powered by AMD’s next-generation Instinct GPUs, beginning with the MI450 line in the second half of 2026. AMD granted OpenAI a warrant for up to 160 million shares that vests as deployment milestones are reached, starting with the first gigawatt rollout. The deal is expected to be accretive to earnings and represents AMD’s clearest entry yet into hyperscale AI infrastructure. Analysts at Jefferies, DBS, and DZ Bank all upgraded the stock, calling the partnership a decisive moment that positions AMD as a credible alternative to Nvidia for large-scale compute deployments.

Initially, the stock reacted to the prior ATH with a clean fade amid a Nasdaq sell imbalance that fueled profit-taking. The mentioned 211.5-213 key resistance area failed to hold, and the stock closed near the lows.

The following session was mostly consolidation, forming an inside bar as repeated attempts to reclaim 211.5-213 failed. On Wednesday the level was finally flipped and confirmed on a backtest, triggering a sharp move through the ATH.

Tariff headlines later pulled the stock back, and further price action around this area remains key to watch.

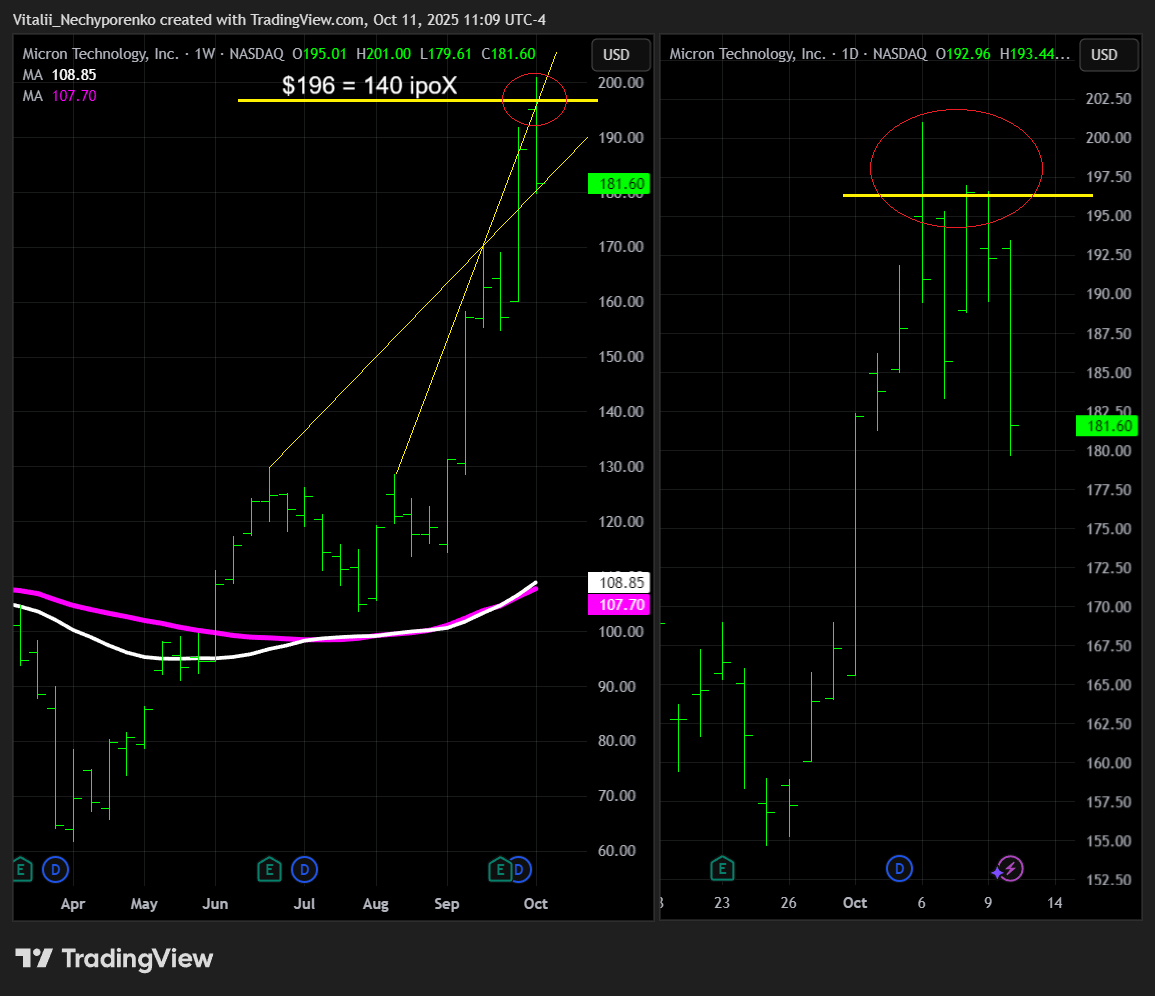

MU -3.32% 1W

Micron drew attention after a wave of bullish analyst actions. Morgan Stanley upgraded to Overweight with a $220 target, Itau BBA initiated at Outperform with $249, and UBS raised its target to $225 citing stronger visibility into high-bandwidth memory demand and a more durable cycle. Shares later turned lower after Sam Mobile reported that Nvidia approved Samsung’s redesigned 12-layer HBM3E chips for its flagship GB300 AI accelerators, marking Samsung’s long-awaited entry into Nvidia’s supply chain.

In the last Weekly Playbook, I highlighted the 196 area as a key level to watch, which also aligns with the 140 IPOx:

With the weekly TRL shifting and 196 now on watch and a bigger resistance standing at 210, fading the rip with calculated risk still looks like the best option.

The stock initially faked higher before reacting sharply to that zone. Attempts to reclaim it later failed, and tariff headlines sealed the move, suggesting a short-term top may be in.

IREN +18.45% 1W

IREN announced new multi-year AI cloud contracts with leading AI firms for Nvidia’s Blackwell GPU deployments. The company remains on track to reach over $500 million in annualized run-rate revenue from 23,000 GPUs operating or on order by Q1 2026, with contracts already covering 11,000 units worth roughly $225 million in ARR. To support this expansion, IREN priced a $875 million convertible notes offering with a 42.5% conversion premium and capped calls up to $120. The company’s rapid transition from ASICs to GPUs and ongoing buildout of its Horizon 1 and 2 data centers highlight its positioning as a key infrastructure partner in the accelerating AI compute market.

The stock was initially rejected at the mentioned 63.75, with a clean backtest of 63 (2.25 IPOx) right before the open on Tuesday, though it managed to reclaim the level and ripped higher in the following sessions amid pricing news. On Friday, it was clearly rejected again at the next mentioned resistance near 70, which also aligns with the 2.5 IPOx level, even before the tariff headlines hit. The stock dropped to 50 afterhours amid heavy volatility, which is not surprising given its retail-driven profile. Further downside remains possible, with limited support until the key 28 area near the IPO high.

GLD +1.01% 1W

Gold drew attention after hitting the major measured-move target from the November 2024 low at 373.28. It didn’t quite reach the large weekly TRL, which appeared to be frontrun by sellers. Although it recovered some losses on Friday, the reaction around this TRL remains an important area to watch.

5. Key Index Charts

In this section I highlight only the most important zones with brief comments. I use fully layered charts to identify them, but keep the charts here clean for clarity.

We can spend days talking about the roaring 2020s, the bull market, rising breadth, a bright future, and the AI revolution, but all it takes is one tweet to flip the tape and send everyone looking for a bid. Literally. I made this meme recently and had no idea I’d be referring to it so soon, though it was clear its moment would come.

Whether we find it on Monday or not is an open question. For now, let’s go to the charts: