MSCI rebalance liquidity rolls straight into March OPEX

AI still drives growth, but SaaS and crowded positioning now demand proof, not promises

The Iran escalation shifts geopolitics from headline risk to real market variable, and the open will reveal who was truly hedged

Last week’s movers: HIMS, AMD, CRCL, CAVA, NFLX, CRWV, DUOL, DELL and XYZ

Earnings to watch this week: ASTS, CRDO, MDB, SE, CRWD, AVGO, VEEV, CIEN, COST and MRVL

Table of Contents

Market Overview

Key Index Charts

Earnings & Interesting Movers Recap

Earnings to Watch This Week

1. Market Overview

Quick housekeeping note before we dive in:

The public test period for Price Action Playbook: Research has officially ended.

Thank you to everyone who participated. Access is now limited to paid subscribers, with a few additional precision fields added, nothing that turns this into a signal service.

Also, for clarity, there are no Discord, Telegram, or WhatsApp groups where I provide trading signals. If anyone contacts you claiming otherwise, block and report.

Markets closed the week lower, but the bigger story was not the red candles. It was the reaction function. Earnings remain strong, yet price action is skeptical. Beats are being absorbed rather than rewarded. The tape is no longer asking whether growth exists. It is asking whether growth justifies the multiple. That shift alone explains most of the volatility.

The week opened with a sharp risk off tone tied to renewed tariff uncertainty and intensifying AI disruption fears, then swung into a technical rebound that briefly restored footing before fading again. It was active, but not constructive. Friday’s MSCI quarterly rebalance added real liquidity into the close without producing clean dislocations. Events like this matter more than most realize. With the first major quarterly expiration in March approaching, positioning into that third Friday will shape liquidity and volatility. The expiration itself matters, but the gamma reset after it often matters more. If you are not familiar with how these dynamics impact opening and closing auctions, you should be. There has been plenty written about it. It is not theory. It shows up in price.

NVIDIA became the cleanest expression of the current regime. Another strong report, record data center revenue, bullish guidance, and yet the stock sold off hard. This was not just fundamentals. Sentiment and positioning were heavily skewed into the event. When everyone leans to one side, the market tends to punish that side first. The issue is not whether AI demand exists. It is whether hyperscaler capital spending remains durable, whether competition compresses future returns, and whether the current capital intensity can justify the valuation already embedded in the stock. Earnings estimates continue to rise, but multiples are not expanding meaningfully. That tension defines this tape. In a crowded trade, even a beat can become liquidity.

SaaS remains the emotional battleground. Automation headlines reignited fears that agents will displace traditional platforms, then integration messaging triggered a rebound. What is dead may never die, but that does not mean it escapes scrutiny. The group is not being priced for extinction, yet it is clearly not being priced for easy multiple expansion either. It is being priced for proof. With CrowdStrike, MongoDB and Veeva reporting into this backdrop, guidance and tone will matter more than headline beats. The market already knows the disruption narrative. It wants evidence that AI enhances margins rather than compresses them, and in a crowded tape, the reaction may matter more than the numbers.

The Netflix episode fits the same capital discipline filter. The stock had been carrying deal risk, with investors modeling a debt heavy acquisition layered on top of an already competitive environment. When Netflix stepped away, the stock ripped. The breakup fee was incremental. The real signal was restraint. In a regime where multiples are capped and scrutiny is rising, avoiding balance sheet risk can be as bullish as delivering growth. NVIDIA is being asked to prove returns on AI capex. Netflix was rewarded for not chasing scale at any cost. Different sectors, same discipline.

Geopolitics now becomes the evolving variable. The U.S. strike headlines hit after the equity close, so markets have not yet had a full session to digest the implications. Hedging was already elevated into the weekend, and crypto began selling off immediately as an early signal of risk appetite. Futures may open deeply in the red on Sunday. Whether that dip becomes opportunity or acceleration is up to the market, not us.

Iran’s direct production footprint is meaningful, but the real sensitivity sits in the Strait of Hormuz, a chokepoint that handles roughly a quarter of seaborne crude and major LNG flows. Even without full closure, heightened threat levels can raise insurance costs, delay shipments, and inject a risk premium into energy. Limited disruption can move prices. Broader escalation that touches infrastructure or neighboring producers is where oil scenarios begin to matter for global growth and inflation. For now, this is not a priced outcome. It is a developing distribution.

The week ahead brings PMI data, the jobs report, and a meaningful SaaS slate. In a market that has been range bound for months despite rising earnings estimates, the reaction to numbers will matter more than the numbers themselves. With quarterly expiration approaching and geopolitics now layered on top, volatility remains the mechanism. If futures open sharply lower, some will try to fade it. If you do, mind your stops. This tape punishes complacency faster than it rewards conviction.

2. Key Index Charts

In this section I highlight only the most important zones with brief comments. I use fully layered charts to identify them, but keep the charts here clean for clarity.

NVDA didn’t provide any real clarity, and the new question is how futures will open today after the strikes on Iran. We’ll leave that open for now. In the meantime, let’s go to the charts.

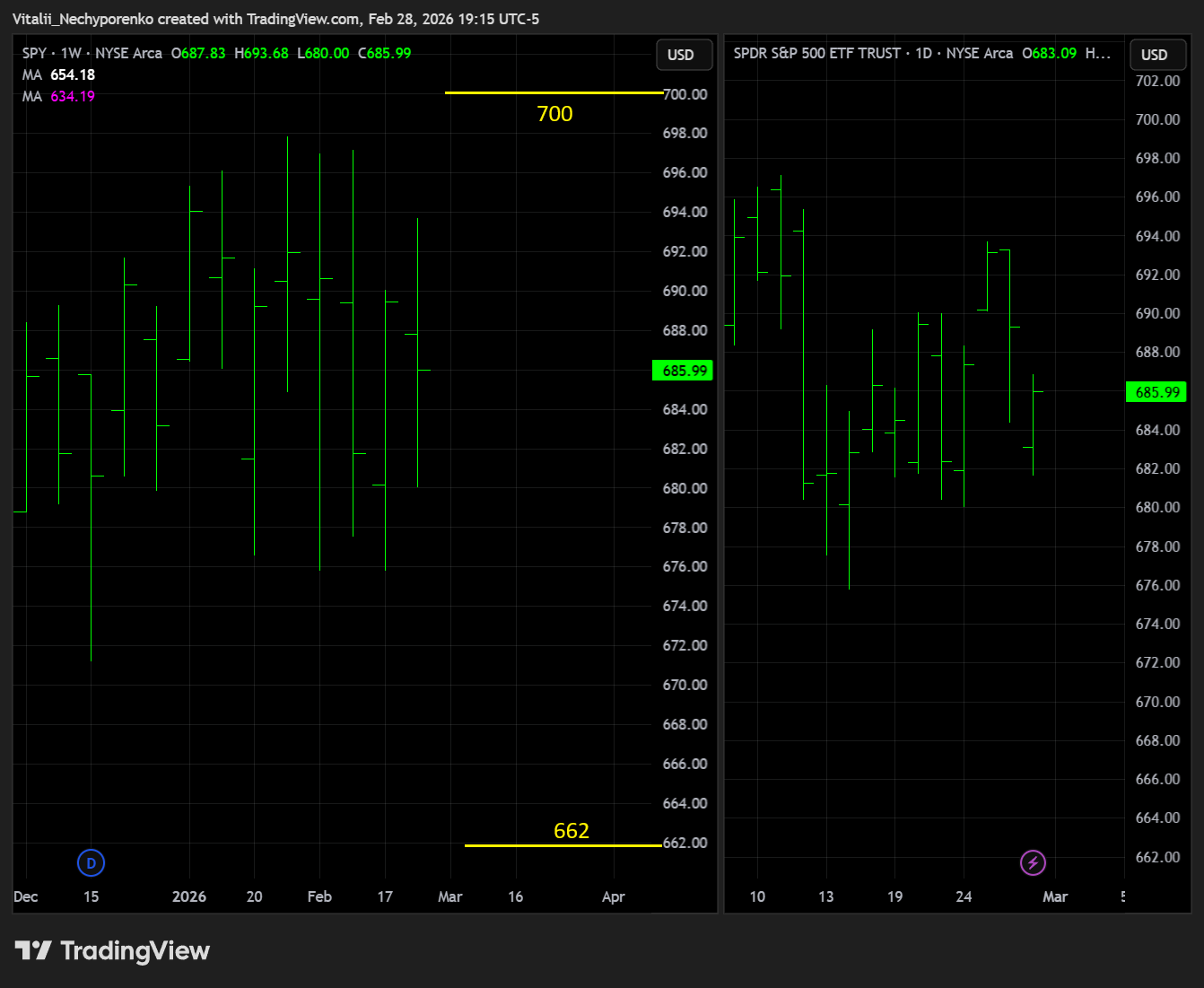

SPY

The S&P 500 ETF continues to trade back and forth, and like any consolidation, a resolution will come sooner or later. Key resistance remains intact at 700, while key support shifts to 662, in case things get really ugly on Monday.

QQQ

The Nasdaq 100 ETF looks similar, but weaker. With NVDA and hedging activity likely behind it, let’s see where we go from here. Key resistance also remains intact at 626, while key support shifts to 580, and it better hold.

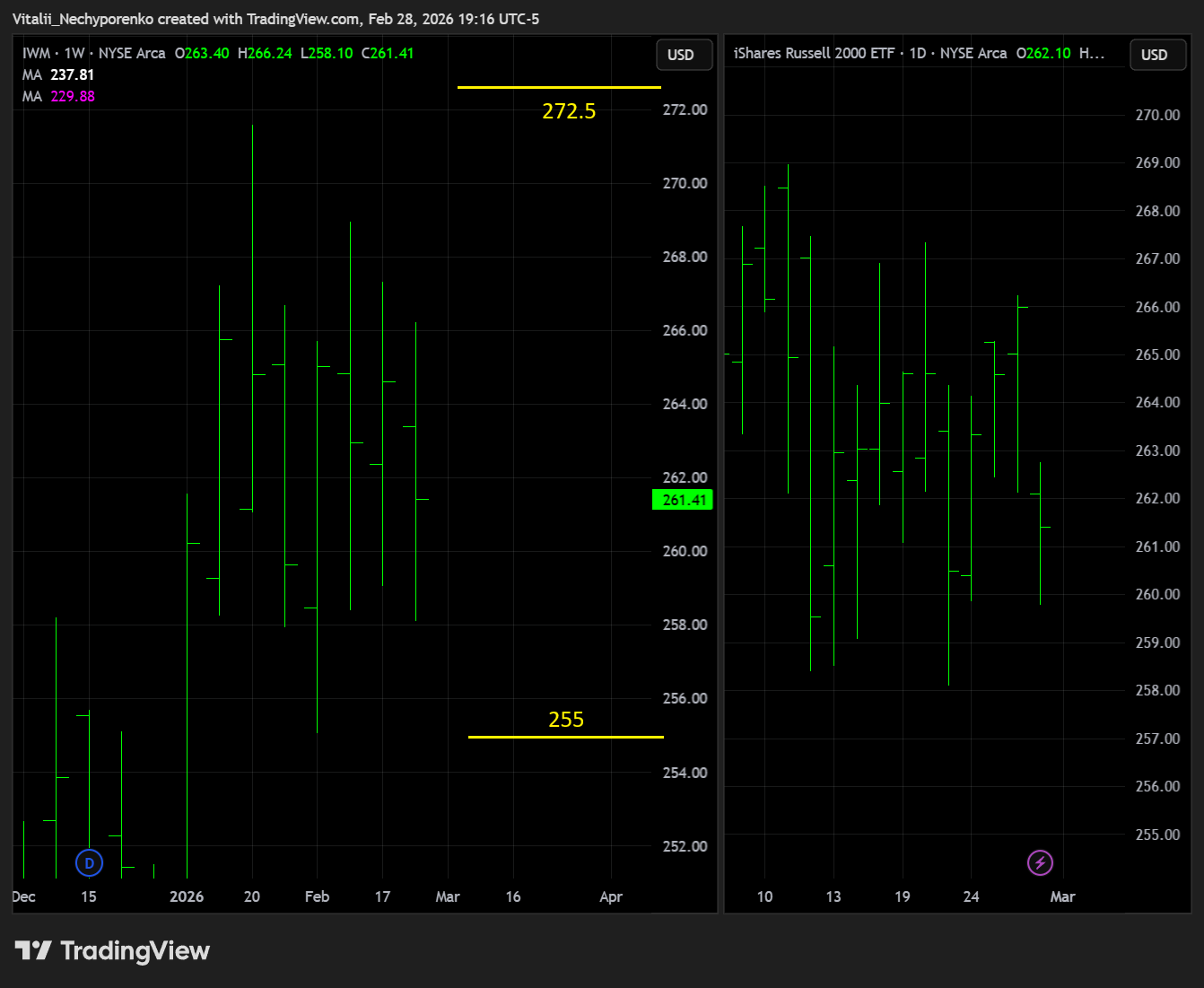

IWM

The Russell 2000 ETF is showing healthy consolidation despite weakness on Friday, and the DTL breakout remains on watch. Key support stays intact at 255, while key resistance shifts slightly higher to 272.5.

TLT

The 20+ Year Treasury Bond ETF is ripping higher, and the reaction to key resistance at 92 is on watch. Key support remains intact at 88.

BTC

Bitcoin did make a higher low at the right spot (prior key support that was undercut when price touched 60k), though the lack of any meaningful bounce adds one more question to the mix. If bulls finally give up, the next key support area sits around 55k, while key resistance shifts lower to 74k.

ETH

Ethereum looks similar, with both key support at 1600 and key resistance at 2200 remaining intact.

DXY

Dollar will no longer be covered on a weekly basis and will be dropped from this section going forward. If something material develops, I will address it.

3. Earnings & Interesting Movers Recap

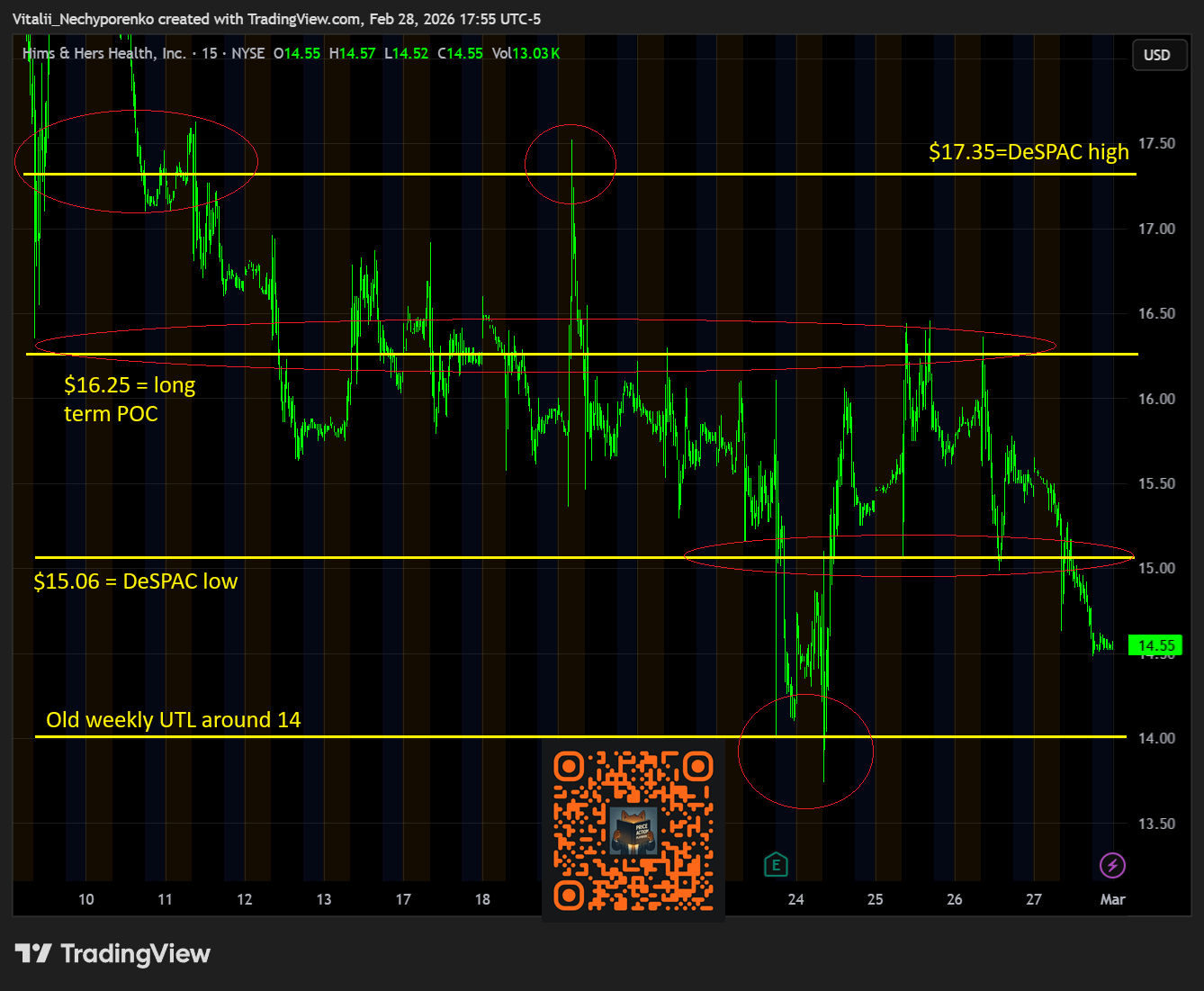

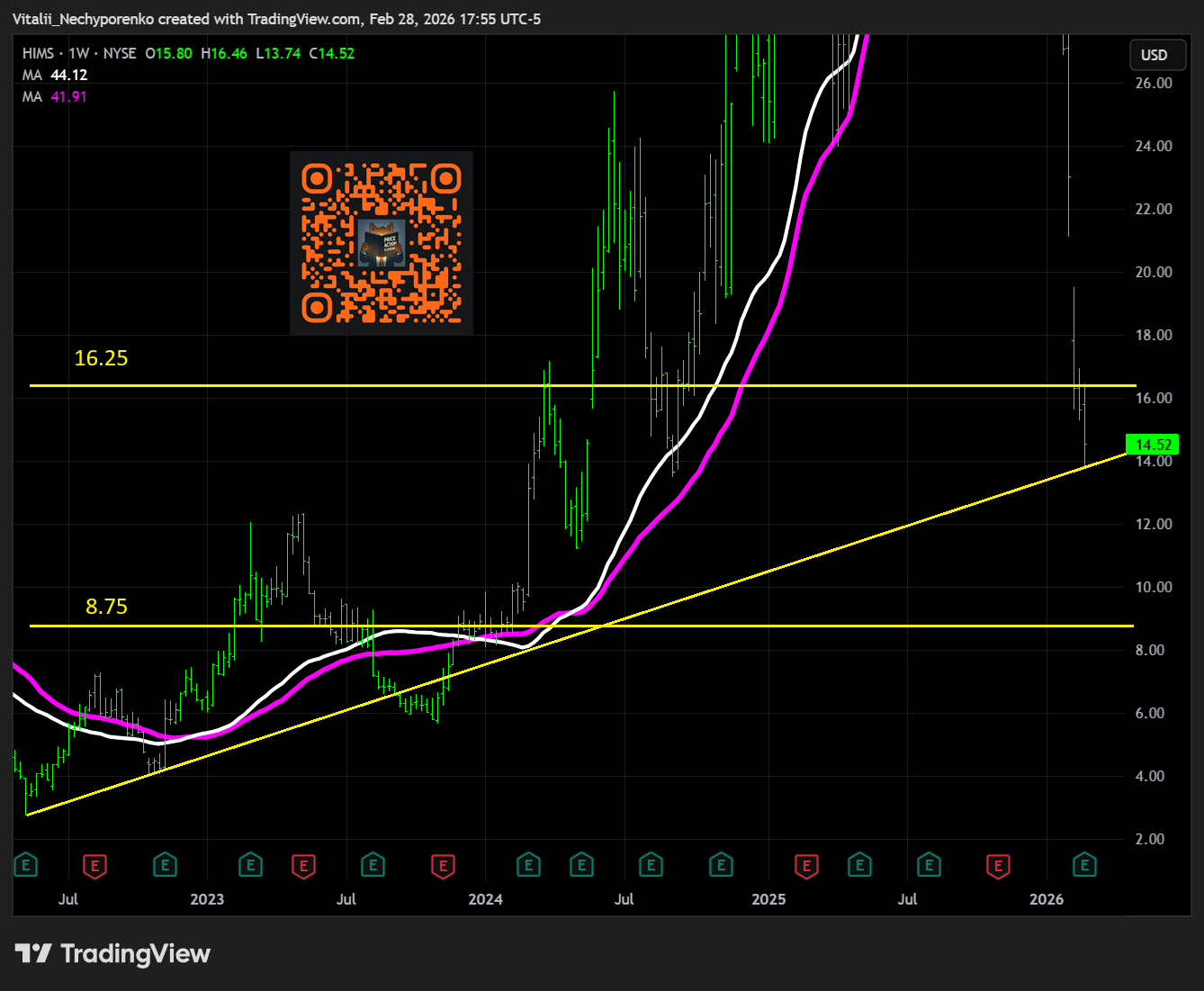

HIMS

Hims & Hers Health reported Q4 revenue of $617.8 mln, up 28% YoY, with adjusted EPS of $0.08 modestly ahead of expectations, but the quarter was overshadowed by softer guidance and emerging regulatory overhang. Subscriber growth remains strong at more than 2.5 mln users, reflecting continued expansion across hormone therapies, diagnostics, and international markets, yet profitability momentum appears to be moderating. Adjusted EBITDA of $66.3 mln rose 23% YoY but trailed some buy-side expectations, and Q1 revenue guidance of $600-625 mln implies a meaningful sequential slowdown versus consensus near $653 mln. Full-year FY26 revenue guidance of $2.7-2.9 bln was broadly in-line with consensus but below more bullish estimates, with management signaling a back-half weighted growth profile. Incremental scrutiny around GLP-1 offerings, shipping cadence adjustments, and broader regulatory risk adds uncertainty at a time when growth durability is being reassessed. Execution against diversification initiatives and clarity on legal exposure will be central to sustaining investor confidence in the platform’s long-term trajectory.

I think I highlighted the three key areas to watch well before the numbers hit the tape. The fourth is an old weekly UTL that, once defended, led to heavy short covering. The interesting part is that despite vicious buying, price could not hold above 16.25, which is probably the most important level among them, being the long-term POC for the stock. The near-term future of the stock will be defined by this fearsome foursome, and the key question is how many shorts are left willing to cover here. If the answer is not many, the next very important POC sits at 8.75.

AMD

Advanced Micro Devices announced a multi-year AI infrastructure agreement with Meta Platforms to deploy up to 6 gigawatts of custom MI450 and Helios systems, a contract estimated at $60-100 bln over five years and one of the largest wins in the company’s history. The deal materially expands AMD’s footprint within hyperscale data centers, with initial 1-gigawatt shipments expected to begin in 2H26, implying a revenue ramp into late next year and beyond. As part of the structure, AMD issued performance-based warrants for up to 160 mln shares, roughly 10% dilution, vesting against shipment milestones and stock price targets, introducing a meaningful tradeoff between long-duration demand visibility and shareholder dilution. Strategically, the agreement positions AMD as a core partner in Meta’s AI buildout, though it remains unclear whether the capacity meaningfully displaces Nvidia or primarily supplements Meta’s aggressive scaling plans. Margin implications and pricing discipline will be central, as the balance between securing anchor hyperscaler volume and preserving long-term profitability now defines the debate.

I think the importance of the 225 zone was highlighted multiple times, so let’s focus on structure here. The area is formed by 57.5 IPOx, a prior weekly pivot high, and a prior weekly TRL. The way it flipped from resistance to support and back is clearly visible on the daily chart as well. Everything else is in the books, and it seems like this particular bear market assassination attempt failed. It might take something more Advanced and less Micro to succeed.

CRCL

Keep reading with a 7-day free trial

Subscribe to Price Action Playbook to keep reading this post and get 7 days of free access to the full post archives.