Table of Contents

Market Overview

Earnings to Watch This Week: ORCL and ADBE

Research Unpacked: IBM, NOW, HPE, MRVL, AVGO, CRWD and LULU

1. Market Overview

Weekly Playbook structure is changing.

I’d like to call it an evolution, but we’ll see.

Starting this week, Key Index Charts are being removed. They will continue to live in Price Action Playbook: Research, where they originate anyway. From time to time, individual index charts may still appear in the Market Overview section when something particularly interesting is worth highlighting.

To make up for it, Earnings to Watch This Week is now fully open to everyone. Knowing which area was highlighted is useful. Understanding the logic behind it is where most of the value lives.

Stay tuned.

Leebowski wanted 5% of Ethereum. Walter Saylor spent years explaining why Bitcoin should never be sold.

Treasury companies spent the last couple years raising money to buy crypto, raising more money to buy more crypto, then raising even more money to explain why buying crypto had become a business model. Crypto Spring. The Alchemy of 5%. Preferred shares. Convertible notes. Staking yields. Unrealized gains. Unrealized dreams. Somewhere between the first treasury announcement and the latest preferred offering, the entire crypto sector wandered into a bowling alley and never really left.

Everybody seems to know where the money is. BitMine already controls roughly 4.5% of Ethereum and Walter Saylor accumulated more than 843,000 Bitcoin. Treasury companies trade at premiums. Analysts publish higher targets, at least they used to. Investors buy the companies that buy the assets. The briefcase keeps changing hands and the numbers keep getting bigger. Apparently somebody kept the money.

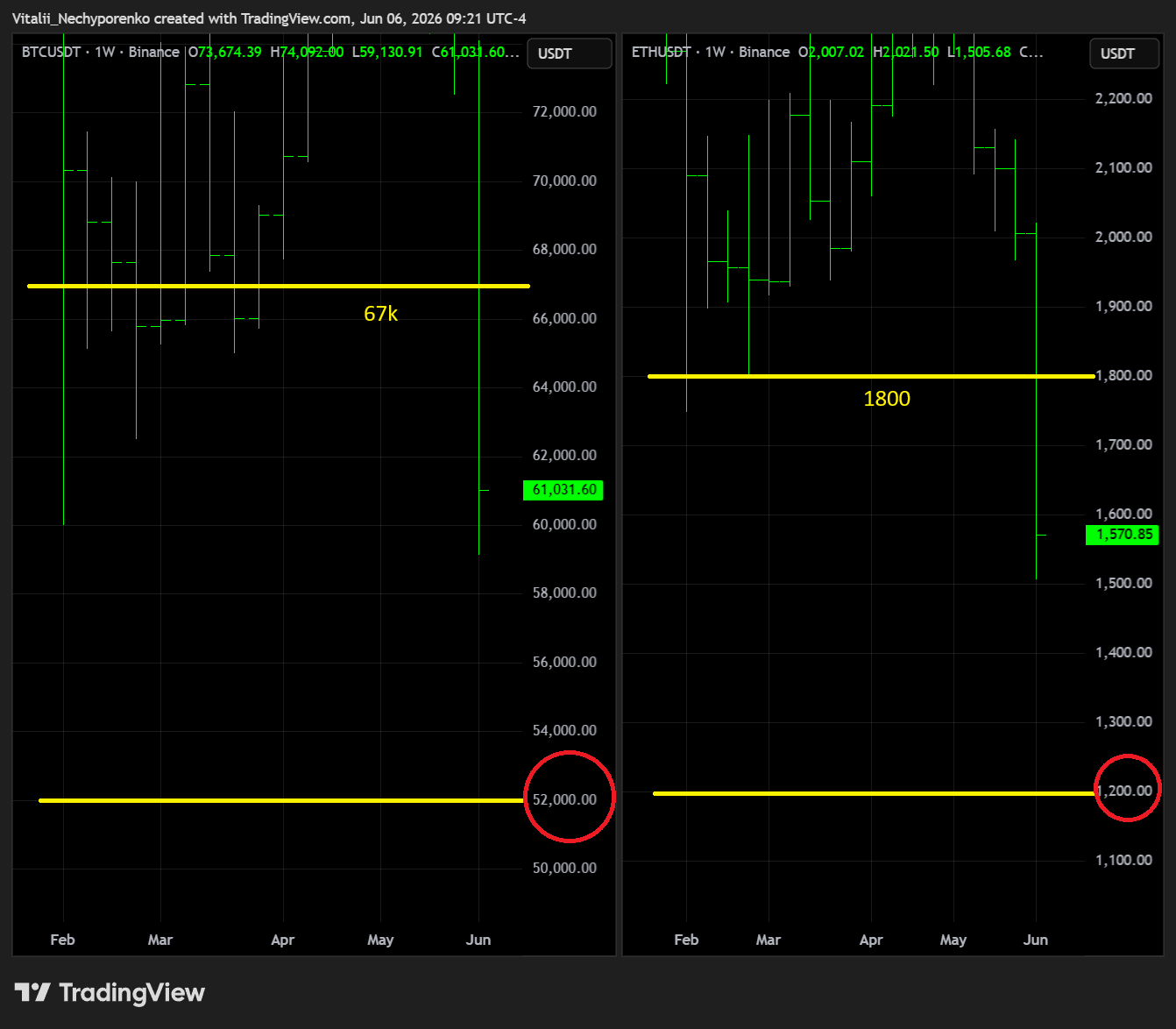

BTC failed to hold 67k, ETH flushed through 1800. Those levels shouldn't come as a surprise by now. Next big supports sit at 52k and 1200. The lower it goes, the louder the margin calls. Will they answer this time?

The crypto crowd spent most of the cycle debating adoption, tokenization, decentralization and institutional participation. Then the conversation shifted toward outflows, positioning and liquidity. Long-term theses remained largely untouched. Market structure had other plans. The Dude abides. Markets don't.

Crypto increasingly trades like a high-beta destination for speculative capital rather than some isolated alternative universe. Everybody wants the money. The briefcase just doesn’t stay in one place forever.

Owning Bitcoin or Ethereum stopped being enough. The trade evolved into owning companies that owned Bitcoin and Ethereum, and eventually into owning increasingly elaborate structures wrapped around those same assets. Wall Street took crypto speculation, securitized it, repackaged it and then started layering additional speculation on top of the securitized speculation. Mark it zero.

Walter Saylor finally sold Bitcoin. Not much Bitcoin, just thirty-two coins, just enough to fund preferred stock distributions. Years of “never sell” collided with preferred holders who apparently enjoy getting paid. And while Bitcoin doesn’t care, preferred shareholders generally do.

Leebowski took the idea in a different direction. More than 5.4 million ETH and more than 4.7 million staked. A public objective of controlling 5% of Ethereum’s entire supply. Validator infrastructure, OpenAI exposure, staking businesses, treasury assets and preferred offerings paying 9.5% suddenly found themselves living under the same roof. New capital raised to acquire additional ETH. Additional capital raised against accumulated ETH. Projected staking revenues used to justify further expansion. At some point it became difficult to tell where the Ethereum story ended and the financing story began. Then somebody starts asking where the money comes from and whether the machine works in reverse. Suddenly there are questions about dilution, access to capital, financing costs and perpetual accumulation models. Has the whole world gone crazy? Apparently there were rules after all.

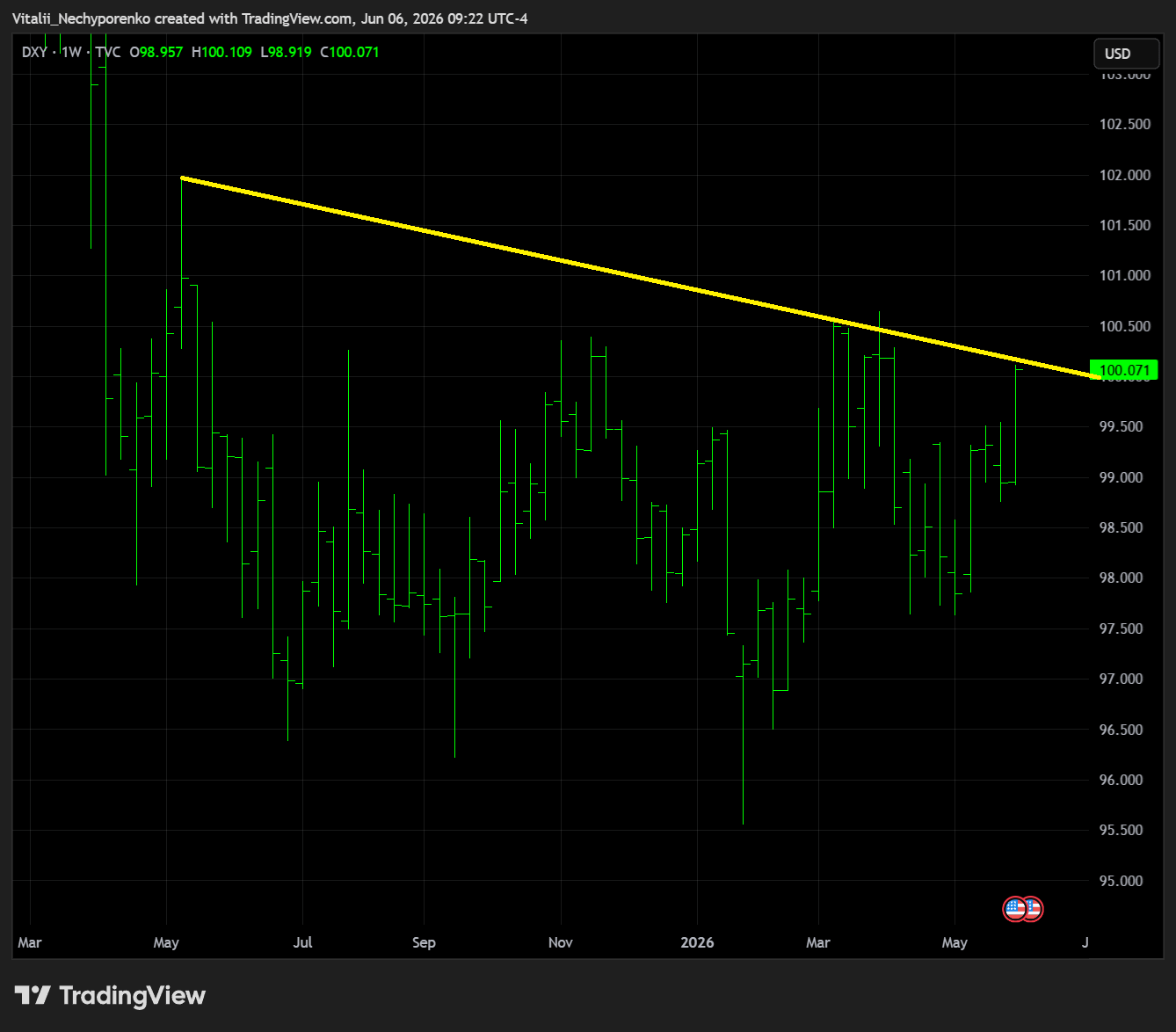

For all the attention BTC 100k received, DXY 100 may have been the rug that tied the room together:

A stronger payroll report pushed higher-for-longer fears back into the conversation and helped the dollar find its footing again. Rate expectations shifted, DXY marched back toward the century mark and risk assets responded accordingly. By Friday the selling had expanded well beyond crypto. The S&P 500 snapped its nine-week winning streak, the Nasdaq suffered its worst week since April 2025 and suddenly the market looked a lot less interested in funding every story with a ticker attached.

Leebowski once suggested that the next stock market pullback would feel like a bear market.

But which pullback didn’t?

2. Earnings to Watch This Week

In this section I share clean charts highlighting only the key areas used for planning and execution. The levels are identified using fully layered charts, but are presented here without the extra clutter.

All levels reflect Friday’s close and serve as a roadmap rather than a prediction. If a key area is in play before earnings, the focus shifts to the next relevant zone.

That’s not inconsistency. That’s price action.

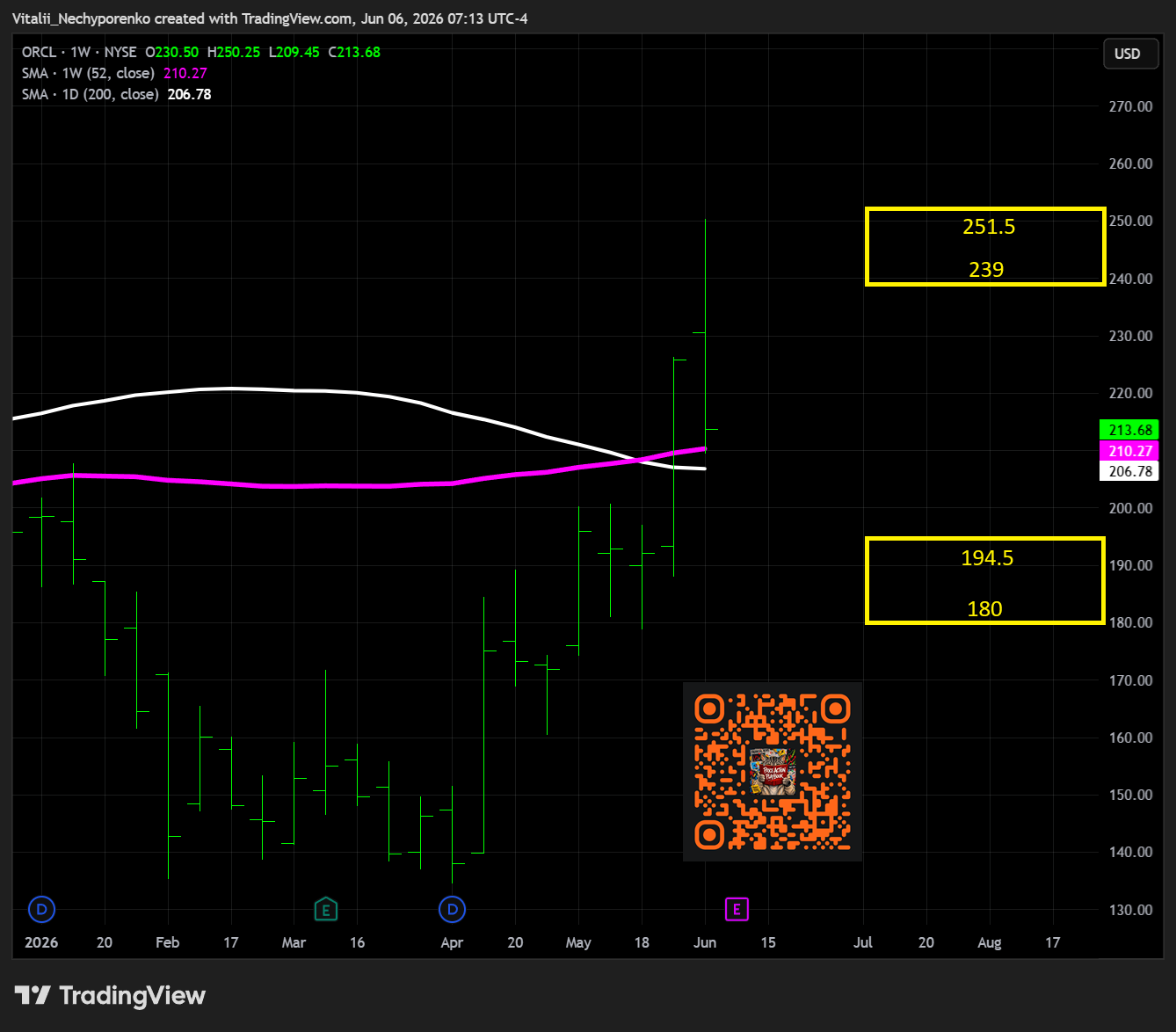

Wednesday

ORCL

EPS Timing: After Market Close

Turnover: $5.1 billion

Support: $180-194.5 (Projected move to support: -8.98%)

Resistance: $239-251.5 (Projected move to resistance: +11.85%)

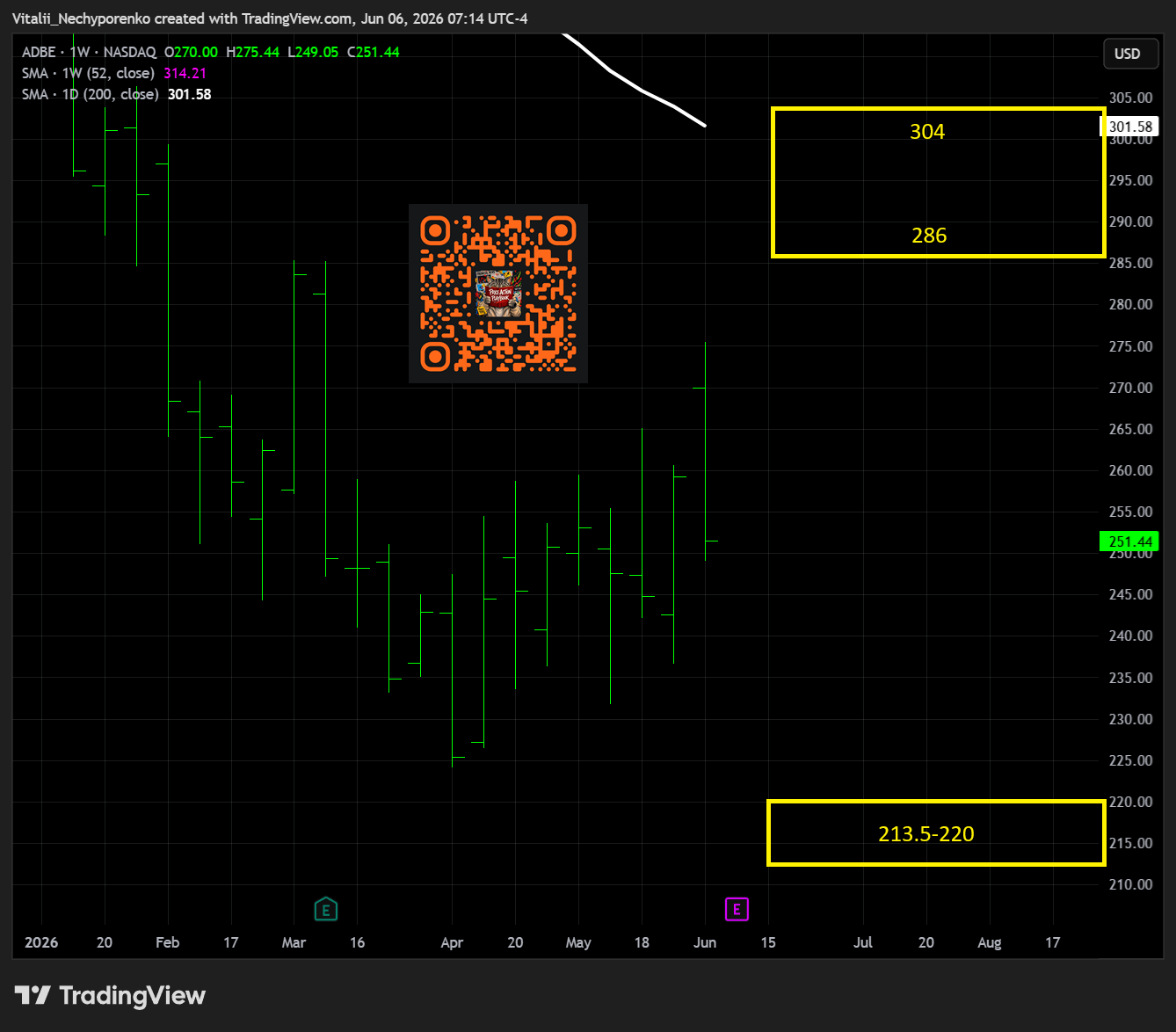

Thursday

ADBE

EPS Timing: After Market Close

Turnover: $1.3 billion

Support: $213.5-220 (Projected move to support: -12.50%)

Resistance: $286-304 (Projected move to resistance: +13.74%)

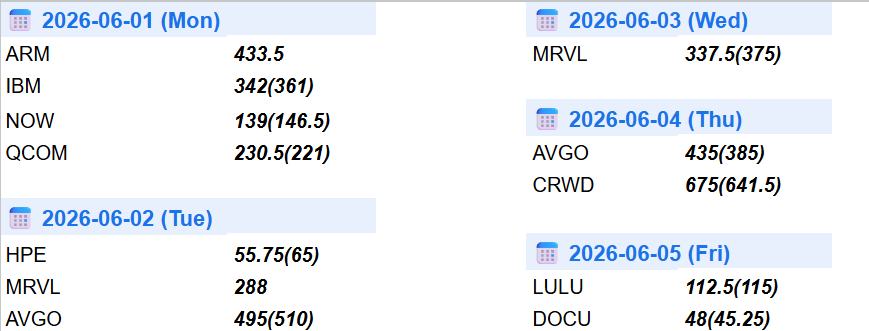

3. Research Unpacked

Below is this week's Price Action Playbook: Research dump

Let's look at the logic behind some of those areas: