Weekly Playbook: January 5th

Breaking news from Venezuela probably won’t break anything

Key Takeaways This Week

Geopolitical headlines may shake futures, but markets remain driven by AI earnings and capital flows

Earnings season will test how much optimism is actually priced in

Earnings to watch this week: APLD and STZ

Table of Contents

Market Overview

Playbook Podcast Spotlight

Key Index Charts

Earnings to Watch This Week

1. Market Overview

Quick housekeeping before we dive in:

A batch of complimentary subscriptions will be gifted tomorrow morning, which should be timely with earnings season picking up. Full details are outlined in the note below

Also, if you missed it, we published a new Crypto Playbook deep dive focused on BNB:

The extraction of Nicolás Maduro may qualify as breaking news, but it is hardly news that breaks anything. Headlines can sound seismic, yet markets rarely care unless they interfere with earnings, liquidity, or capital allocation. Oil can twitch and futures can gap, but it still takes more than regime change in Venezuela to derail a tape powered by AI spend and forward growth assumptions. To actually break this market, you would need something closer to Jensen Huang being escorted out by Delta. Short of that, markets move on.

And move on they did. The close of 2025 told a familiar story. Major indices finished the year with strong gains, followed by mild profit taking into a holiday shortened week. The S&P 500 wrapped the year up roughly 16% and ended just off record highs despite a 1% pullback in the final stretch. Nasdaq added close to 20% on the year, though it logged its fifth straight daily decline into year end, a reminder that momentum does not glide forever. Financials lagged as positioning unwound, with banks acting less like leaders and more like ballast.

The broader tone remains relaxed, almost complacent. Volatility sits near the lower bound of its multi year range, supported by expectations of continued rate cuts and confidence that AI driven profit growth will paper over most macro noise. That calm is precisely what makes the setup more fragile. After three consecutive years of double digit gains, history argues for moderation. Forward returns tend to compress, and volatility tends to rise, especially when markets are priced for execution rather than resilience.

This is where earnings season reenters the frame. The first real catalyst arrives with bank results in mid January. Financials matter not because they define growth, but because they validate or challenge assumptions about credit, deal flow, and economic durability. Any hint of slowing loan demand, softer M&A pipelines, or cautious guidance would ripple quickly through the broader index, given how tightly financials remain correlated with the S&P 500. The second catalyst follows shortly after, with the Federal Reserve decision later in the month. A pause or a less accommodating tone would reprice rates and equities together.

Through all of this, the AI trade remains the dominant axis. It is entering its fourth year and still delivering. Demand for data center hardware remains firm into the first half of 2026, with order books extending well beyond that. Memory constraints are forming, inference workloads are scaling, and capital continues to circulate through hyperscalers and private markets alike. At the same time, the risks are becoming clearer. Financing saturation, hyperscaler digestion, and most importantly power availability are no longer abstract concerns. They are constraints that will shape the next phase of growth rather than accelerate it.

That is why geopolitics, for all its noise, remains secondary. Oil reserves do not set multiples. Earnings do. Capacity does. Execution does. Markets can absorb a surprising amount of political theater as long as the growth engine keeps running.

The rest period is over. The calendar has flipped, liquidity has returned, and the work resumes. January will not be quiet. Expectations are high, margins for disappointment are thin, and real catalysts are back on the schedule. This is no longer a market to drift through. It is a market to engage with deliberately, one earnings report at a time.

2. Playbook Podcast Spotlight

3. Key Index Charts

In this section I highlight only the most important zones with brief comments. I use fully layered charts to identify them, but keep the charts here clean for clarity.

Time to forget about Santa and turn the focus to geopolitics and the upcoming earnings season. The first trading session of the year was volatile, but one data point is not enough to draw conclusions, no matter how hard some try to do exactly that. With that in mind, let’s get to the charts:

SPY

The S&P 500 ETF disappointed recent ATH breakout buyers, though this may prove to be nothing more than a shakeout. Key resistance shifts lower to 693, aligning with the fresh TRL, while key support remains at 674.

QQQ

The Nasdaq 100 ETF tagged the key support at 610 on Friday that was highlighted last week before a modest snapback. The next key support area to watch sits at 602, while key resistance shifts lower to 625.

IWM

The Russell 2000 ETF saw some buying on Friday, which is a constructive sign. A break above the recent daily DTL would be encouraging, though the real test still sits at the key resistance at 255. Key support remains intact at 244.

TLT

The 20+ Year Treasury Bond ETF saw solid selling pressure, closing near its pivot low and effectively answering the question of whether it could flip the 200d. While 86.5 may still act as a reactive area, the next key support sits lower at 85.25. Key resistance remains intact at 88.25.

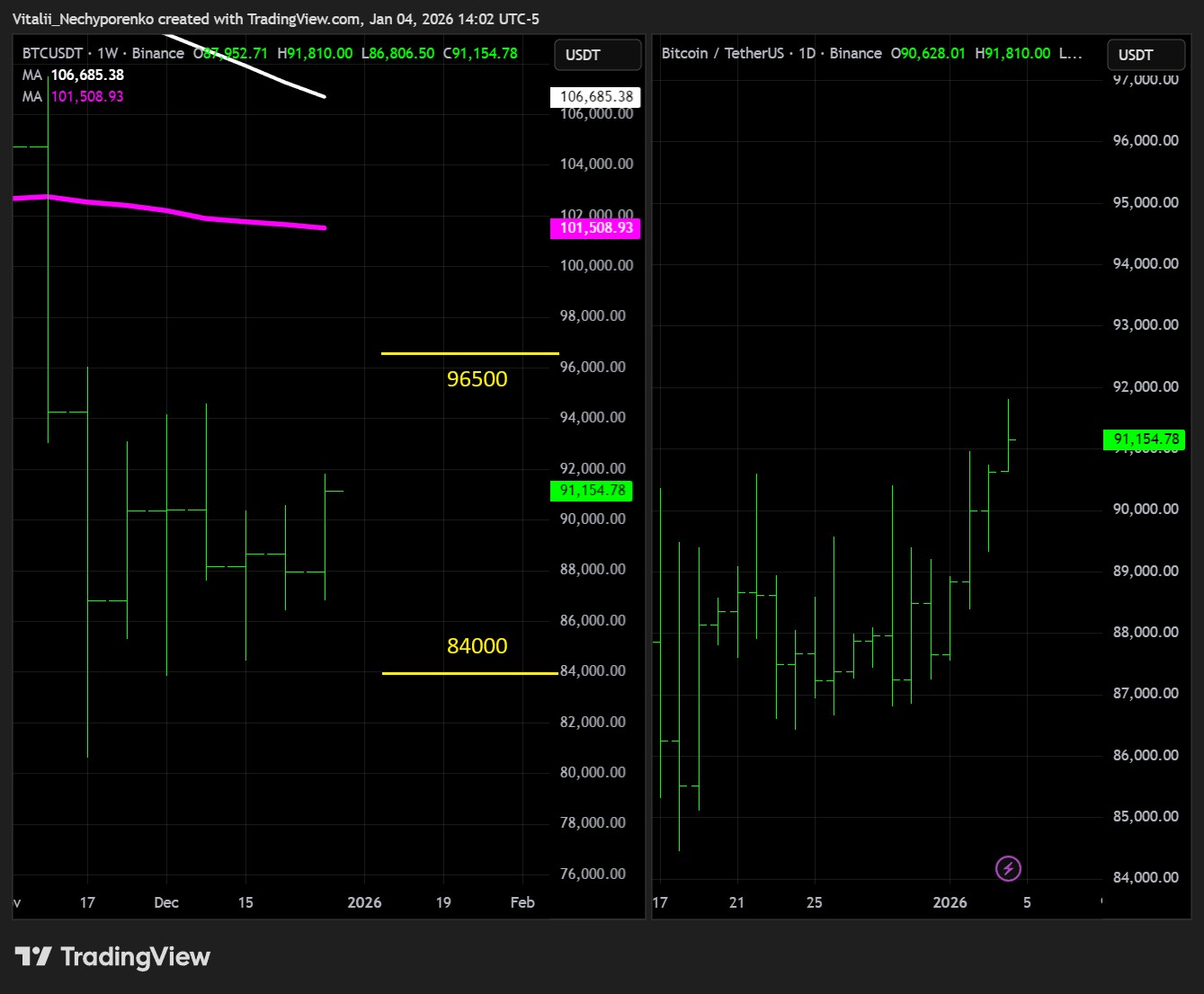

BTC

Bitcoin and the crypto overall may have picked a direction, though confirmation is still needed. The reaction at the key resistance near 96500 is the main focus, while key support shifts to 84000 and it needs to hold, especially given the recent inflows(of overleveraged crowd?😁).

ETH

Ethereum largely mirrors Bitcoin, though it managed to reclaim and hold above the 3100 level highlighted last week, which looks more constructive. The next major test is whether it can clear key resistance at 3500, while key support shifts to 2900 and needs to hold as well.

DXY

Dollar caught some bids, and it will be worth watching whether recent geopolitical developments add to that momentum. Key support shifts slightly lower to 96.5 in line with the trendline angle, while key resistance remains intact at 99.25.