Key Takeaways This Week

Reclaim is easy when positioning is offside, holding is the real test.

Earnings season is coming, and not everything moving is alive.

Last week’s movers: CF, UNH, DAL and APLD

Earnings to watch this week: GS, JNJ, JPM, ASML, TSM and NFLX

Table of Contents

Market Overview

Key Index Charts

Earnings & Interesting Movers Recap

Earnings to Watch This Week

1. Market Overview

Quick housekeeping note before we dive in:

On Tuesday, during JPM’s conference call kicking off earnings season, full access pricing goes up ~25%. If you’re already in, your pricing stays locked.

Full access includes Weekly, Lucky Quarter, Crypto, and Market Mechanics Playbooks, plus Research where the gameplan, key levels, and earnings prep live.

Everything is built around price action, structure, and execution. If you’ve been watching from the sidelines, this is your window.

The war ended in the weirdest of ways. A cease-fire headline, a big and beautiful victory declaration, and the tape flipped immediately, pushing markets straight back into prior structure and reclaiming levels that just failed days ago. The move looks clean on the chart, but underneath it feels less like recovery and more like something being pulled back to life.

The rally was sharp and aggressive, with the Nasdaq up roughly 4.7% and the S&P around 3.6% on the week, driven primarily by semis and AI, which continue to dominate leadership and push back toward highs. That strength stands out, but the path there matters more than the result. This was not a gradual rebuild, it was a reset driven by positioning. Oversold conditions met a headline catalyst, shorts were forced to cover, underexposed longs were pulled back in, and price stopped searching for bids and started chasing them. In the span of a few sessions, the tape moved from oversold to overbought without building anything in between, advancing quickly but without the structure that usually supports a move meant to last.

Now we are back inside the old structure, but nothing has been resolved yet. These levels already failed once, and reclaiming them is only the first step. They now need to be defended and held, otherwise this becomes just another round trip rather than a new leg higher. The recent tape makes that question more complicated because participation is far from broad. The market is not buying everything, it is buying what already worked. High-beta names, semis, AI leaders are being chased again, while more stable, fundamentally solid names are either ignored or sold. The advance is narrow and relentless, pushing higher through the same names, almost mechanical in the way it moves.

Call it rotation if you want, but it looks more like concentration returning faster than structure can support it.

The TACO narrative fits neatly into this dynamic, with headlines once again driving the move, but the more important signal is how little time price spent building acceptance. Levels were skipped rather than tested, and moves extended quickly without consolidation. Once that repositioning is done, the market is left with a vacuum, and that is where momentum either finds real sponsorship or starts to fade once the forced buying is gone.

That is where the setup starts to show its fragility. After a move like this, price has to hold on its own. If it can build above these reclaimed areas and spend time there, structure starts to repair. If not, the same levels that just flipped back into support can quickly turn into supply again, just from a different group of participants who missed the first move or are looking to exit into strength.

Macro isn’t providing an anchor either. Oil remains a central pressure point despite the sharp reversal, with supply still tight and inflation dynamics not fully resolved, while recent data continues to show elevated headline inflation driven by energy. Growth is holding but not accelerating, and the Fed remains in a wait-and-see mode, which leaves the market without a clear policy anchor. Across assets, confirmation is still lacking, with equities rallying sharply while other signals remain mixed, reinforcing the idea that this is still a positioning-driven environment rather than a fully aligned trend.

That’s where things shift. Earnings season is coming.

Financials will set the initial tone, and expectations are not weak. Results are likely to be supported by trading and investment banking activity, even as sentiment around the group has remained cautious. That divergence between solid fundamentals and hesitant positioning is the real setup going into the first wave of reports. The key question is not just whether companies beat expectations, but whether the market is willing to reward those results and, more importantly, how guidance shapes the forward outlook, especially around credit quality, consumer strength, and exposure to less transparent areas like private credit.

Tech faces a different test, with growth expectations still elevated and largely centered around AI-driven demand. The numbers themselves matter, but the reaction matters more. If strong reports lead to sustained moves and participation broadens, it would suggest that the recent rally has a foundation to build on. If leadership remains narrow and even good results fail to hold gains, then the underlying issue has not changed, and the market is simply revisiting the same imbalance from a different level.

Other themes continue to build in the background. AI adoption is accelerating across both institutional and retail workflows, compressing research cycles and shifting how decisions are made, but without necessarily creating a consistent edge. At the same time, structural pressures such as rising deficits and higher interest costs remain in place, shaping the broader environment even if they are not driving day-to-day price action.

The move was strong and the reclaim was real, but strength driven by repositioning is easier to achieve than strength built on acceptance. The market has done the first part, the second is still missing, and until that changes, this kind of advance can keep pushing higher without ever fully proving itself.

Earnings season is coming, and that is where this move either finds real buyers or runs out of air.

2. Key Index Charts

In this section I highlight only the most important zones with brief comments. I use fully layered charts to identify them, but keep the charts here clean for clarity.

Something got brought back a little too fast. The recent tape suggests a lot of participants were caught off guard by the latest round of TACO moves, with aggressive short covering pouring fuel on the move as positioning flipped and traders chased leaders while dumping laggards. It’s fast, narrow, and a bit too clean for something that just broke structure.

The question hasn’t changed: once the forced buying fades, does this hold, or does it fall apart just as quickly?

SPY

The S&P 500 ETF gapped above the previously mentioned resistance at 662 and never looked back. That level has now flipped into key support and needs to hold, while resistance shifts higher to 688.

QQQ

The Nasdaq 100 ETF also gapped above 599, which now serves as key support for the overall structure, while resistance stands at 621.5.

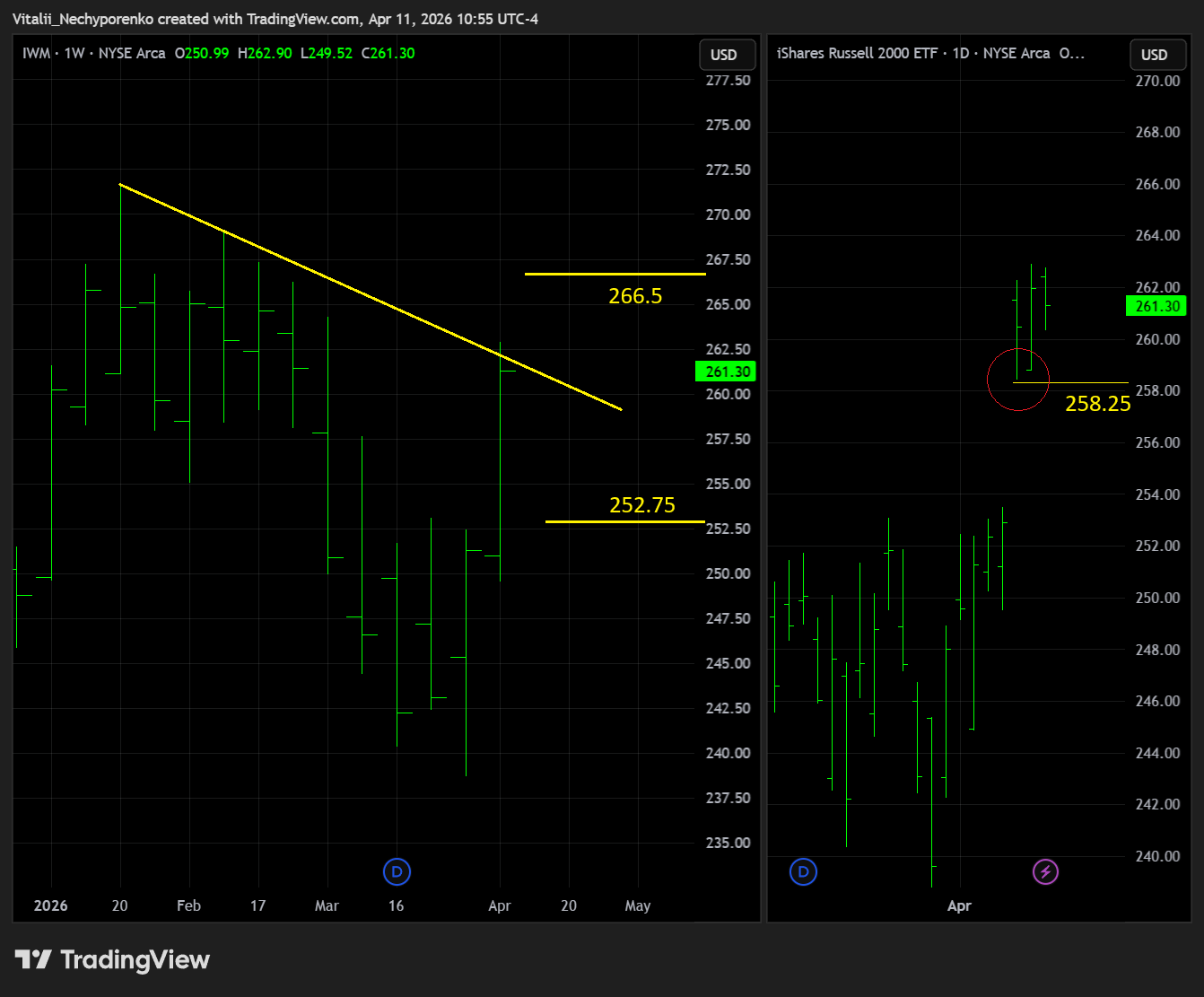

IWM

The Russell 2000 ETF came the closest to testing the mentioned key resistance on the flip and passed the test. The next level to watch sits at 266.5 if it clears the fresh weekly DTL. It still ranks best in terms of overall setup, with key support at 252.75.

TLT

The 20+ Year Treasury Bond ETF didn’t do much, with key resistance remaining intact at 88.50, while support shifts slightly lower to 85, aligning with the weekly BSL angle.

BTC

Bitcoin is starting to look better after 2 months of sideways consolidation, now approaching its key weekly DTL. Whether this time is different remains to be seen. Key resistance shifts to 79k, while support moves higher to 67k. Crypto, fingers crossed.

ETH

Ethereum looks very similar and ready for action. Key resistance shifts higher to 2525, while support moves up to 1925.

3. Earnings & Interesting Movers Recap

CF

CF Industries was a notable mover this week as fertilizer markets reacted to shifting dynamics around the Strait of Hormuz, where geopolitical tensions initially pushed nitrogen pricing higher before reversing on cease-fire developments. While oil remained the primary focus, the region plays a critical role in global nitrogen supply, making CF particularly sensitive to disruptions across Iran, Qatar, Saudi Arabia, UAE, and Egypt. Early in the week, supply concerns supported pricing, but sentiment shifted quickly as a two-week ceasefire agreement and the prospect of resumed passage through the Strait reduced immediate risk, pressuring fertilizer prices and resetting expectations around near-term supply constraints. The move reflects how tightly CF’s outlook is tied to geopolitical developments, where pricing can rapidly swing between supply shock and normalization, leaving fundamentals highly dependent on stability across key export routes.

This one came on the radar from the imbalance lists, and the setup was purely imbalance-driven, though the fact that it coincided with a prior reactive weekly TRL breakdown only added fuel to the fire. Call it a quick warm-up before the season, but the reference price shifts and late snowballing orders were too tempting to ignore. Add the catalyst on top, and you have a clean recipe for an opening auction dislocation. More on the topic:

Unraveling the Open: Premarket Structure and Imbalances on NYSE and AMEX

For each listed security, there is a single official opening price published by the primary listing venue. That price is the same for every market participant, regardless of where orders were placed overnight, which venue was used, or how fragmented premarket trading appeared. It does not emerge organically from early prints and it is not negotiated after the fact. It is established deliberately, through an auction designed to reconcile supply and demand into a unified starting point.

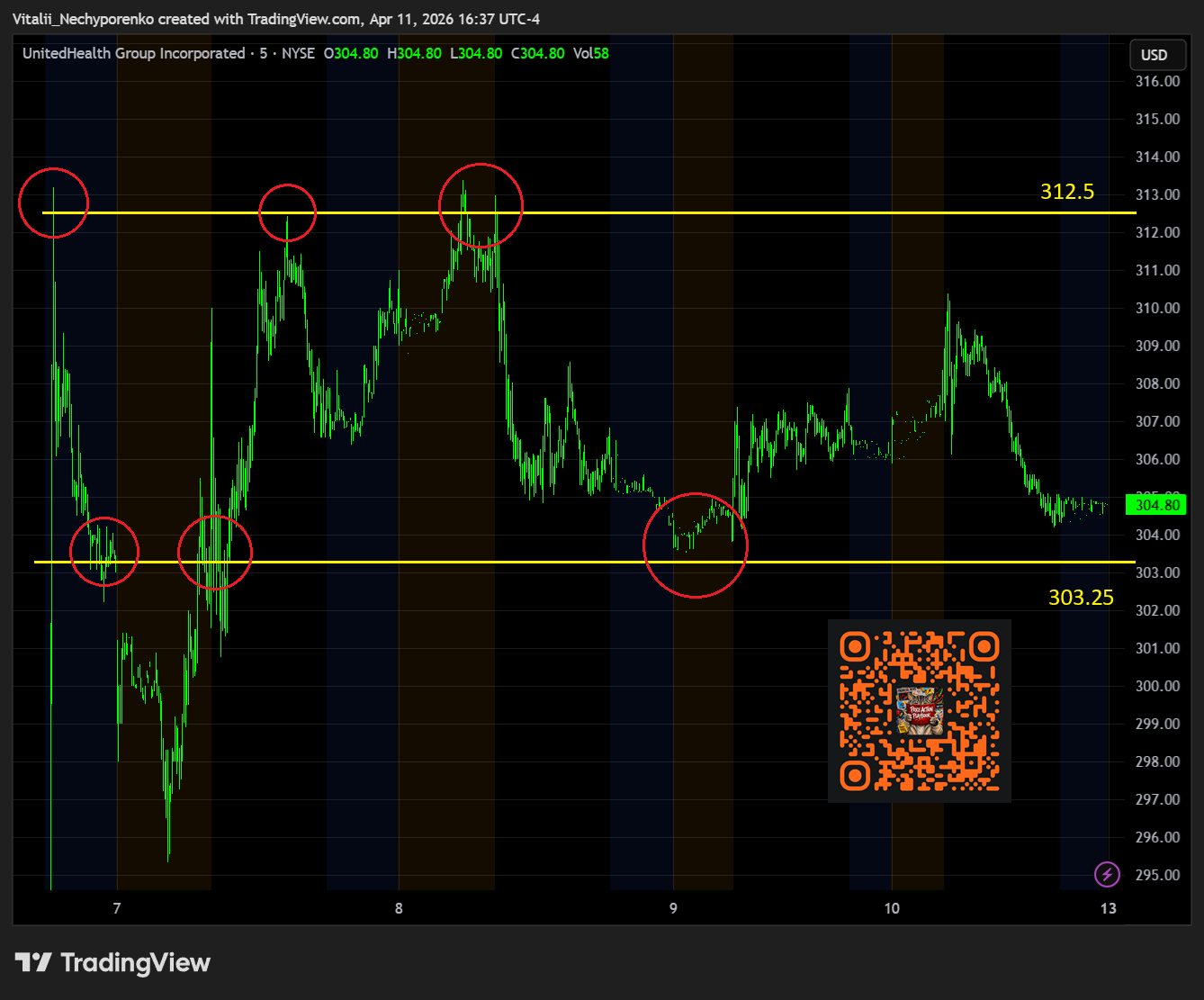

UNH