SOL 2026: The High-Performance Backbone of Consumer Crypto

How execution speed, capital velocity, and real usage define Solana’s role in the current cycle

Welcome to the next edition of the Crypto Playbook, a series of focused deep dives into digital assets that function as market infrastructure rather than short term narratives. Previous editions examined Bitcoin as the monetary anchor of the crypto ecosystem, Ethereum as the settlement and compute layer of Web3, and BNB as an integrated execution and distribution platform. This edition turns to Solana.

This report examines Solana as a high performance execution layer built for consumer oriented crypto use cases. We focus on how architecture, on chain activity, token economics, developer dynamics, and competitive positioning fit together after multiple stress tests and a full market cycle. The objective is not to revisit past narratives, but to evaluate Solana based on what it does today and why it continues to attract real usage.

As always, the goal remains the same. Keep the analysis concise yet comprehensive, grounded in structure and observable behavior rather than ideology, and focused on the dynamics that matter for investors, traders, and analysts who view crypto networks as operational infrastructure, not speculative stories.

Introduction

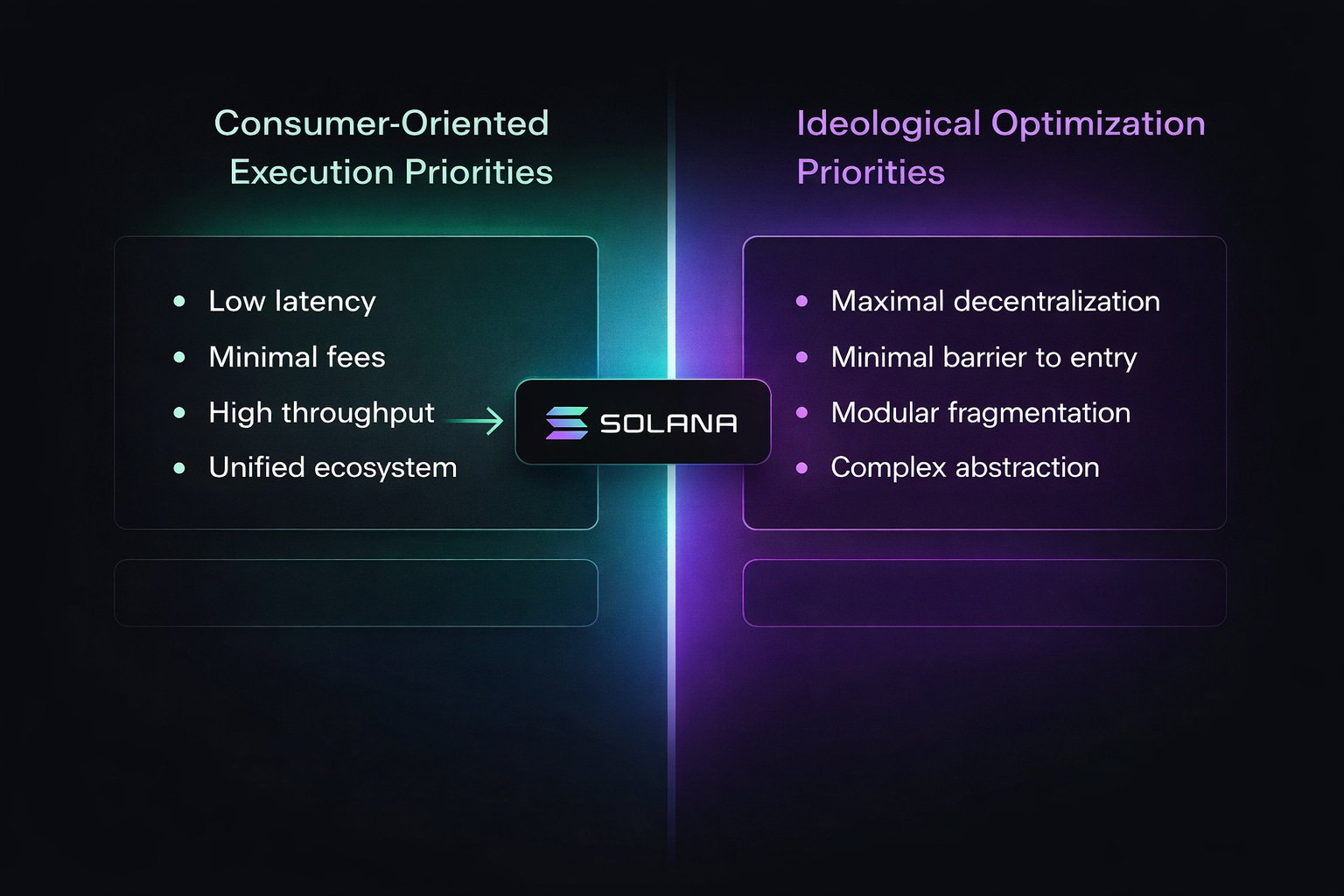

In 2026, Solana is no longer positioned as an “Ethereum killer.” That framing belonged to the 2020-2021 cycle and ultimately proved methodologically flawed, as it reduced blockchain comparisons to ideological opposition while ignoring differences in target use cases. Solana’s current role is fundamentally different. It is a consumer grade L1 optimized for mass usage rather than for maximizing abstract decentralization metrics.

The primary reason Solana deserves attention today is visible in empirical on chain data. During 2024-2026, the network consistently shows high transaction volumes, a large number of active addresses, and clear dominance in high frequency on chain usage segments. This activity is not the product of temporary subsidies or centralized incentives. It is driven by genuine demand from users and applications for which low latency and minimal fees are critical.

A second fundamental factor is the post-FTX stress test. The collapse of FTX and Alameda Research in 2022 removed several key pillars from the Solana ecosystem, including liquidity, market making, and informal institutional support. For many L1 networks, such a shock would have been fatal. Solana not only maintained basic functionality but gradually restored ecosystem activity. This suggests that the network’s current state is based on organic viability rather than reliance on an external backstop. From an investment perspective, this materially reduces the risk of illusory growth that characterized the previous cycle.

The third element is a broader shift in market priorities. In the current cycle, the crypto market has moved away from the theoretical maximization of decentralization and toward practical infrastructure characteristics. The dominant criteria are now user experience, execution speed, transaction costs, and the ability to serve mass demand without fragmentation.

Within this framework, Solana is not a compromise solution. It is a direct reflection of market demand. Its architecture does not attempt to satisfy all ideological requirements simultaneously. Instead, it is optimized for a specific class of applications where performance takes precedence over minimizing complexity.

As a result, the relevant question in 2026 is not whether Solana can displace Ethereum, but whether Solana represents the most suitable base infrastructure for consumer oriented Web3 in the current market cycle.

It is within this framework that the following analysis should be considered.

Table of Contents

What Is Solana Today

From Hype to Survival to Product-Market Fit

Technology & Performance Stack

Validators, Consensus & Trade-offs

Tokenomics, Staking & SOL Economics

Fee Market, MEV & Capital Velocity

DeFi, Memecoins & Social Liquidity

NFTs, State Compression & DePIN

Payments, Stablecoins & Mobile UX

Governance, Devs & Institutions

Competitive Landscape

Risks

Growth Scenarios 2026–2028

Conclusion

1. What Is Solana Today

As of 2026, Solana should be viewed as a monolithic, high performance L1 designed with a clear priority on scale and execution within a single base layer. Unlike modular or rollup oriented architectures, Solana does not delegate core functions such as execution, data availability, or settlement to external layers.

All execution logic is contained within a single chain, which minimizes fragmentation and reduces coordination overhead between system components.

This architectural design is optimized around three core parameters:

High throughput. The network is capable of processing large transaction volumes under real world conditions, not merely in theoretical benchmarks. This makes it suitable for high frequency use cases such as trading, memecoins, gaming and social applications, and micropayments.

Low latency. Transaction confirmation time is a critical factor for consumer oriented products. Solana minimizes the delay between transaction submission and finalization, enabling a user experience that more closely resembles Web2 systems than traditional blockchain networks.

Parallel execution. Due to the specifics of its runtime and transaction processing model, Solana can execute independent operations simultaneously. This is a fundamental distinction from sequential execution models and a key reason why network performance scales with demand rather than degrading linearly as activity increases.

Within this context, the SOL token serves several system critical functions. It acts as:

a gas asset required for any on chain operation,

a staking asset that secures the network and underpins validator economics,

the core ecosystem asset used as collateral, a unit of account, and a source of liquidity across most protocols.

Importantly, SOL is not positioned as a deflationary or store of value asset in the classical sense. Its role is to enable the functioning of a high performance execution network. The value of SOL correlates not with scarcity, but with usage intensity and the velocity of capital within the ecosystem.

As a result, Solana today should not be viewed as a universal layer for everything, but as a specialized infrastructure optimized for a specific class of problems where scale, speed, and execution costs are decisive. It is from this perspective that both its strengths and its limitations should be evaluated.

2. From Hype to Survival to Product-Market Fit

The evolution of Solana is best understood through three distinct phases, each of which reshaped both market perception and the network’s underlying economic reality.

2021: the hype phase and the “Ethereum killer” narrative

During the previous cycle, Solana was primarily viewed through the lens of speed and throughput. The market framed it as a technological alternative to Ethereum, often overlooking questions of sustainability, structural dependencies, and genuine demand. A significant portion of liquidity and activity was closely tied to affiliated entities, creating the appearance of organic growth. At this stage, Solana functioned more as a narrative than as a proven product.

2022: systemic shock and survival mode

The collapse of FTX and Alameda Research represented an existential crisis for Solana. The ecosystem simultaneously lost:

key sources of liquidity,

market-making infrastructure,

informal institutional support,

and the trust of a large segment of the market.

This was not merely a bear market, but a stress test of the network’s core design and community resilience. Many projects disappeared, activity declined sharply, and Solana temporarily lost its status as a “serious L1” in the eyes of the market. It was during this period that it became clear that without an external backstop, the ecosystem would either adapt or fail.

2023-2026: organic recovery and the emergence of product-market fit

After the removal of structural dependencies, a slow but strategically critical recovery process began. The defining characteristic of this phase is the nature of the activity itself. Growth is no longer driven by centralized incentives, but by:

real users,

applications with clear demand,

use cases sensitive to transaction speed and cost.

During this period, Solana began to exhibit clear signs of product-market fit across memecoins, high-frequency DeFi, NFTs with genuine trading activity, DePIN, and payments. These segments do not require ideological decentralization as an end goal, but they depend critically on network performance.

As a result, Solana in 2026 is less hype driven but significantly more resilient than it was in 2021. It has lost part of its speculative narrative, but gained something it previously lacked - a proven ability to function in the absence of external support.

From an analytical standpoint, this represents a key transformation. Solana has shifted from being an experiment that “works as long as conditions are favorable” to an infrastructure that has already endured systemic collapse and maintained relevance. This transition forms the foundation for evaluating its role in the current market cycle.

3. Technology & Performance Stack

From the outset, Solana’s technological architecture was designed around a single core objective: maximizing performance within a single base layer. This fundamentally differentiates it from both traditional L1 networks and modern modular stacks, where execution, data availability, and settlement are distributed across multiple layers.

At the core of Solana’s consensus design is the combination of Proof of History (PoH) and Proof of Stake (PoS). Proof of History is not a standalone security mechanism, but a cryptographic time source that allows events to be ordered without constant coordination among validators. This reduces synchronization overhead and enables the network to achieve high throughput without relying on complex external solutions.

A central component of the execution layer is Sealevel, a runtime that supports parallel transaction execution. Unlike sequential models, where each operation must wait for the previous one to complete, Solana can execute independent transactions simultaneously, provided they do not contend for the same state. This is a fundamental architectural advantage that allows performance to scale with demand rather than being constrained by a narrow execution bottleneck.

The result of this design is real world performance in production environments, not merely in theoretical benchmarks. For end users, this translates into:

near instant transaction confirmations,

minimal latency when interacting with dApps,

a user experience that feels closer to Web2 services than to traditional blockchain products.

This characteristic is critical for consumer oriented applications, where even minor delays or unpredictable fees can materially reduce user retention.

At the same time, early versions of Solana’s architecture had a structural weakness - single client dependency. Until 2023, the network effectively relied on a single primary client, increasing the risk of critical failures. This is where Firedancer, an independent client implementation focused on performance, stability, and security, plays a crucial role.

The introduction of Firedancer has several structurally important implications:

reduced single point of failure risk,

improved resilience to bugs and network congestion,

gradual increases in decentralization at the client software level.

Taken together, Solana’s technology stack defines a clear profile: a network that deliberately accepts greater design complexity and higher infrastructure requirements in exchange for maximum performance and superior user experience. This engineering trade off underpins both its current advantages and the future risks that require separate consideration.

4. Validators, Consensus & Trade-offs

Solana’s security model follows directly from its architectural choice to maximize performance within a single layer. This decision has clear implications for validator infrastructure and for the overall level of decentralization across the network.

The first and most visible consequence is high hardware requirements. Participating in Solana validation requires:

powerful CPUs,

significant amounts of RAM,

high network bandwidth,

stable infrastructure with low latency.

This stands in sharp contrast to approaches where validation is possible on minimal hardware. In Solana’s case, a validator is not a hobbyist running a home server, but a professional infrastructure operator. This approach deliberately raises the barrier to entry.

From a design perspective, this is an integral component of a performance first security model. Solana operates under the assumption that:

high throughput,

fast transaction confirmation,

the ability to handle peak load

are critical for a network oriented toward mass usage.

The advantage of this approach is clear. Solana can maintain throughput and stability under load, supporting high frequency use cases that become economically or technically infeasible on more conservative L1s or L2s.

At the same time, this design introduces a clear structural downside - concentration risk. High capital requirements:

reduce the number of potential independent validators,

favor large operators,

may lead to concentration of stake and infrastructure.

This risk is not hypothetical and requires continuous monitoring. However, it is important to note that Solana does not attempt to obscure this trade-off. Unlike networks that claim maximal decentralization while relying heavily on centralized providers, Solana openly accepts complexity and cost as the price of scale.

In summary, Solana’s validator model establishes a clear framework. The network sacrifices simplicity and a low barrier to entry in exchange for performance and scalability. This is not a universally better approach, but it is logically aligned with Solana’s target use cases. Both its strengths and its limitations should be evaluated through this lens.

5. Tokenomics, Staking & SOL Economics

Solana’s economic model fundamentally differs from the narratives that dominated previous cycles around “ultrasound” or deflationary assets. SOL is not designed as a deflationary asset and does not attempt to compete in the store of value category through artificial scarcity. Instead, its tokenomics are structured to support the security and operation of a high performance network.

At the core of this model is inflationary issuance with gradually declining rates. Initial inflation was intentionally high in order to:

incentivize the launch and growth of the validator network,

ensure economic security in early stages,

create attractive conditions for stakers.

Over time, inflation decreases but does not disappear entirely. This means that SOL structurally remains an asset with ongoing issuance, and its long term value cannot be based solely on supply reduction. Within this framework, the value of SOL must be supported by real demand for network usage.

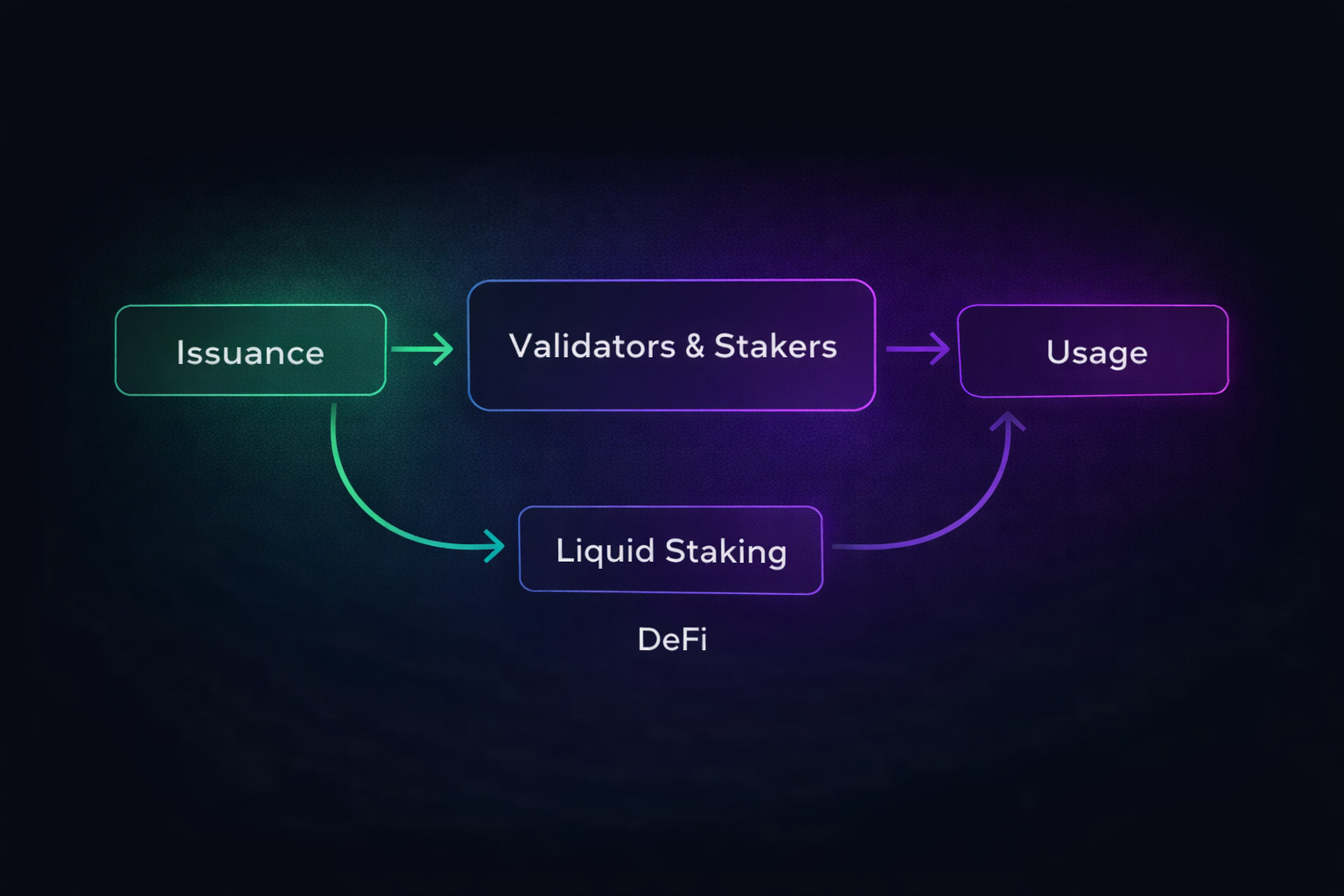

A key component of the economic design is staking. SOL is used to:

secure consensus,

delegate to validators,

generate baseline yield for network participants.

As the ecosystem has matured, liquid staking has become increasingly important. Protocols such as Jito and Marinade allow network security to be maintained while preserving capital efficiency. Staked SOL is not removed from circulation, but continues to be utilized in DeFi, increasing overall capital velocity within the ecosystem.

In this context, SOL should be viewed as a yield plus utility asset:

yield, through staking and MEV optimized reward mechanisms,

utility, through its role as a gas asset, collateral, and base unit of account.

Importantly, SOL’s economics resemble those of an infrastructure token rather than a scarce digital asset. Its sustainability depends directly on on chain activity, transaction volumes, and user adoption, not on mechanical supply reduction.

As a result, SOL is an asset whose value is created through usage rather than restriction. This makes it more sensitive to activity cycles, but also more relevant in scenarios where Solana establishes itself as a high throughput execution infrastructure for consumer Web3.

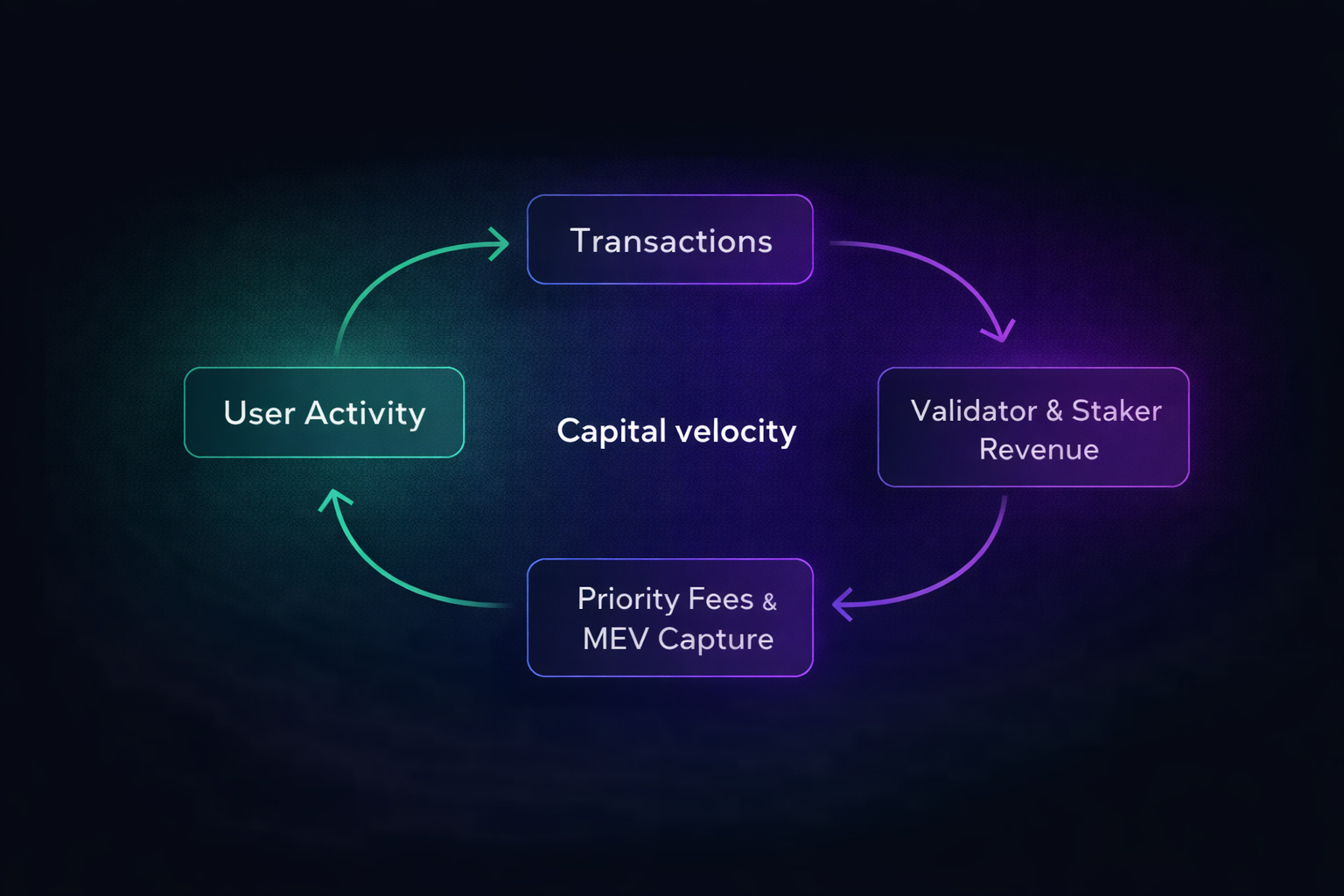

6. Fee Market, MEV & Capital Velocity

Solana’s fee economics fundamentally differ from the fee scarcity logic that dominates the Ethereum ecosystem. Solana does not attempt to turn blockspace into an artificially scarce asset. Instead, it adopts a model oriented toward scale and throughput, where transaction costs are shaped not by global network congestion, but by localized market mechanisms.

The foundation of this model is priority fees. Users and applications can pay an additional fee to prioritize transaction inclusion without increasing the base cost for the entire network. This approach allows the network to:

avoid global fee spikes,

keep simple operations inexpensive,

allocate resources efficiently during peak demand.

Within this system, fees function as an optimization mechanism rather than a barrier to usage.

A core component of validator revenue in this model is MEV (Maximal Extractable Value). On Solana, MEV is not treated as a side effect, but as a structural element of the network’s economy. Protocols such as Jito have introduced auction based models in which MEV:

is transparently monetized,

distributed between validators and stakers,

reduces incentives for destructive practices.

This transforms MEV from a hidden tax into an open market, improving revenue predictability and overall economic resilience.

Memecoins play a particularly important role in shaping this dynamic. While often dismissed as speculative noise, from an economic perspective memecoins perform several critical functions:

they generate massive transaction volumes,

intensify competition for blockspace,

increase both priority fees and MEV.

As a result, rising speculative activity translates directly into validator and staker revenues rather than merely inflating paper metrics such as TVL.

This leads to a key analytical conclusion. Solana is not a TVL maximizing chain. High levels of locked capital are not its primary objective or success metric. Instead, Solana is optimized for:

throughput - the ability to process large volumes of operations,

capital velocity - the speed at which capital circulates through the network.

In this model, network value is created not by how much capital is frozen, but by how intensively that capital is used. This explains why Solana can exhibit high economic activity even in scenarios where its TVL appears modest relative to other ecosystems.

From an analytical standpoint, evaluating Solana through Ethereum style metrics leads to systematic misinterpretations. Solana is a high velocity execution network where economic efficiency is measured by volumes, not by lock ups.

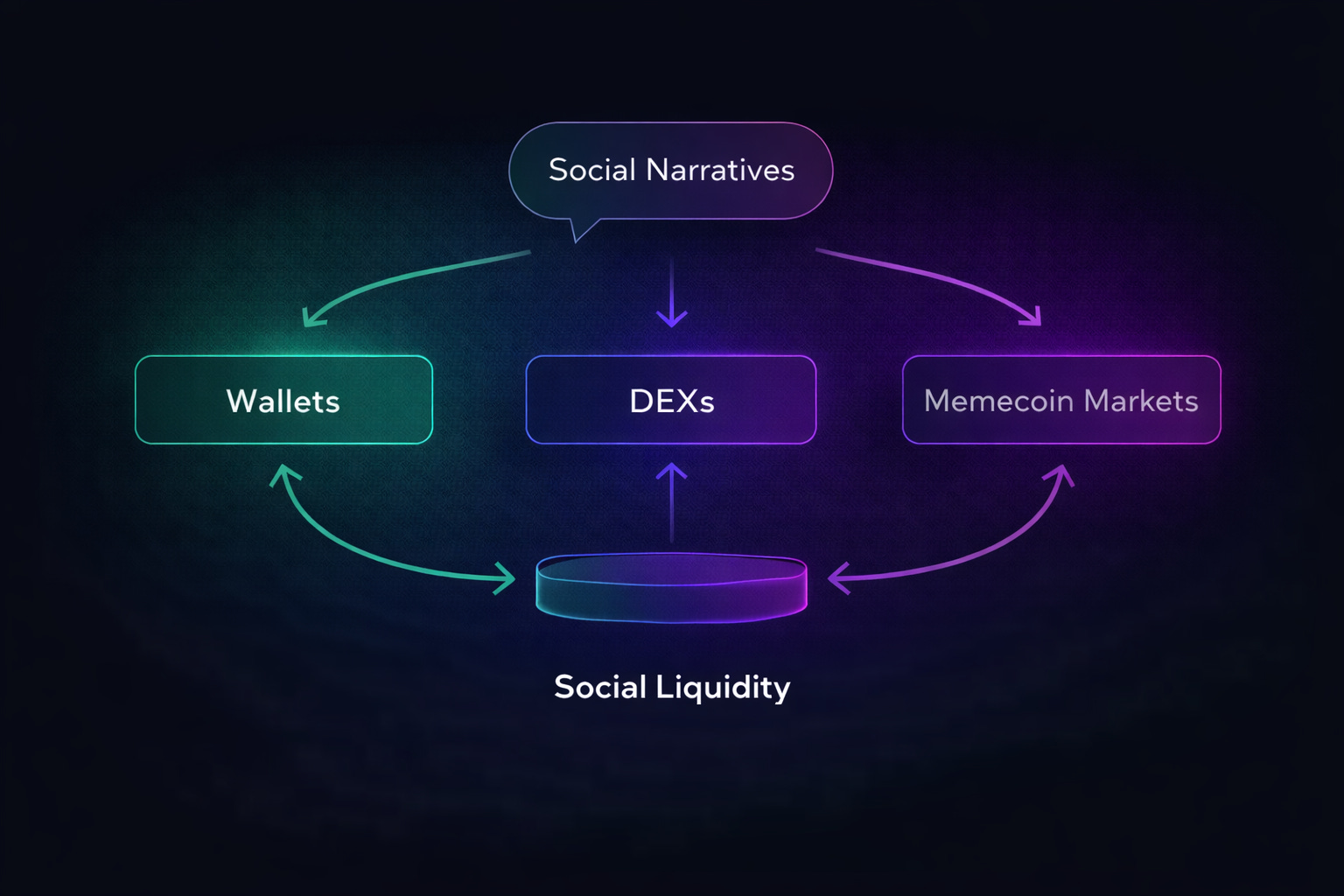

7. DeFi, Memecoins & Social Liquidity

Solana’s DeFi ecosystem operates under a logic that differs fundamentally from the traditional lock up capital paradigm. On Solana, DeFi should primarily be understood as a trading engine rather than infrastructure for long term capital immobilization. Capital within this ecosystem remains in constant motion instead of sitting in a static state.

This dynamic is directly tied to Solana’s architectural properties:

low fees make frequent trading economically viable,

low latency enables high speed execution,

parallel processing removes hard limits on activity scale.

In this environment, DeFi protocols naturally evolve toward liquidity aggregation, order routing, and execution optimization, rather than toward maximizing TVL as an end in itself.

Memecoins play a central role within this model, serving functions that extend well beyond pure speculation. First, they act as an effective user onboarding mechanism. Low friction, minimal fees, and instant swaps lower the entry barrier to levels accessible for mass retail participation. For many users, memecoins represent the first point of contact with the Solana ecosystem.

Second, memecoins create a social layer of liquidity. They merge financial activity with social dynamics such as narratives, communities, and coordination through social platforms. This generates demand not only for the tokens themselves, but also for the underlying infrastructure capable of fast and inexpensive execution.

Third, memecoins function as a source of liquidity and volume. Large speculative cycles generate:

substantial trading volumes,

competition for execution,

rising fees and MEV.

Together, these effects strengthen the network’s economic base, even if part of the activity is short lived.

As a result, Solana has emerged in the current cycle as a center of retail speculation. This does not imply an absence of serious financial or infrastructure use cases, but it does indicate the dominance of high frequency, socially driven activity. From an analytical perspective, this matters. Retail speculation is one of the most powerful drivers of on chain volumes and network effects.

In summary, DeFi and memecoins on Solana form a unified system of social liquidity, where capital, users, and narratives continuously reinforce one another. This dynamic explains why Solana can sustain high levels of activity even during periods when traditional locked value metrics appear unimpressive.

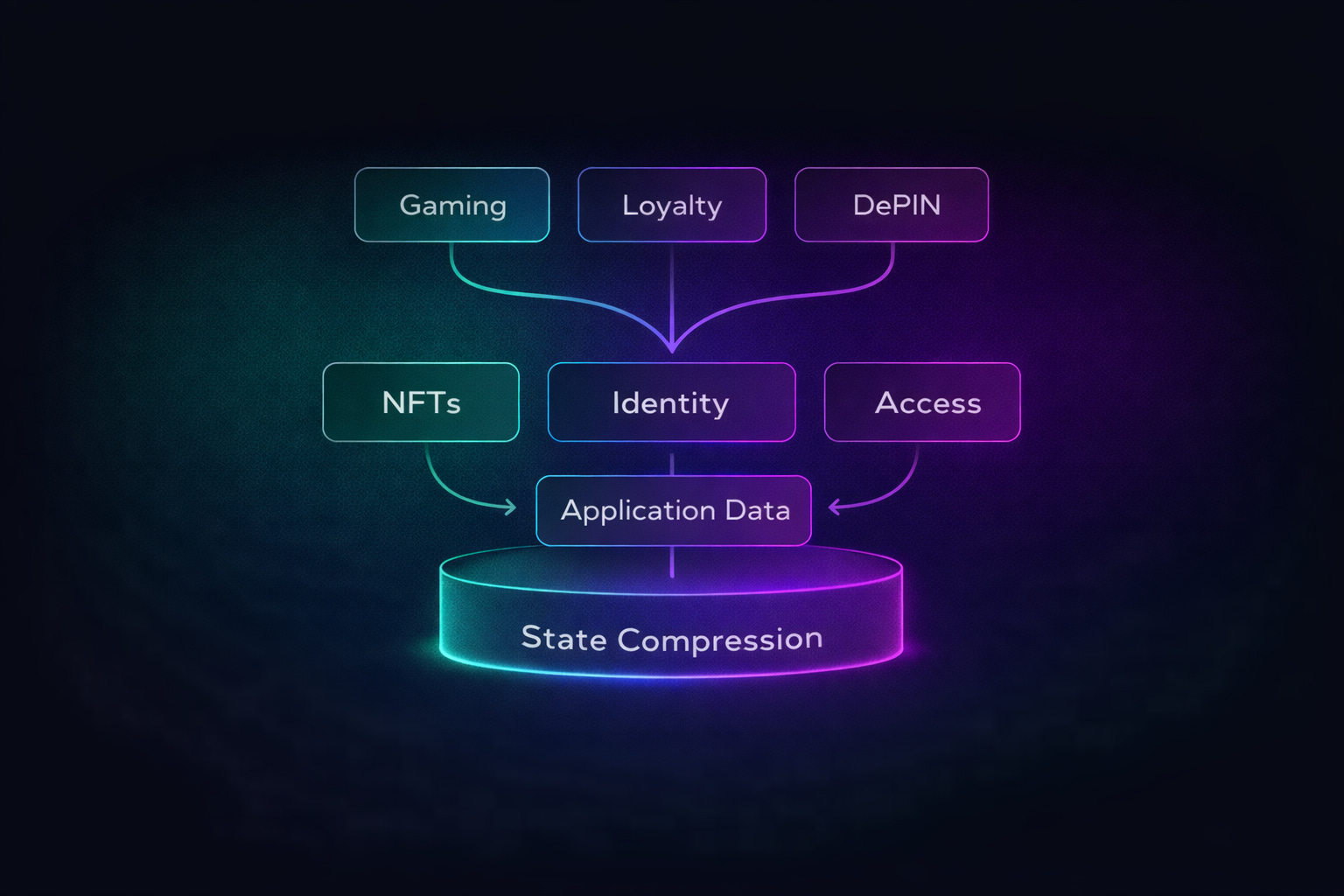

8. NFTs, State Compression & DePIN

Solana’s NFT narrative in the current cycle differs significantly from the speculative model of 2021. The key technological prerequisite for this shift has been state compression, a mechanism that enables large scale storage of NFTs and data assets with minimal on chain state costs.

State compression dramatically reduces the cost of minting and maintaining NFTs, enabling scenarios that were economically infeasible on most L1s:

millions of NFTs,

dynamic data assets,

mass user generated objects.

As a result, NFTs on Solana move beyond narrow speculative use cases and become a functional data layer for consumer applications.

Within this context, NFTs serve several practical roles:

Gaming. Low fees and high throughput allow NFTs to function as fully interactive in game assets with frequent on chain updates rather than static collectibles.

Identity. NFTs increasingly act as carriers of digital identity, reputation, or user status across on chain and off chain systems. The scalability enabled by state compression makes these solutions viable for broad audiences rather than niche communities.

Loyalty and access models. NFTs are used as access tokens, loyalty programs, or membership tiers, where scale and minimal transaction costs are essential requirements.

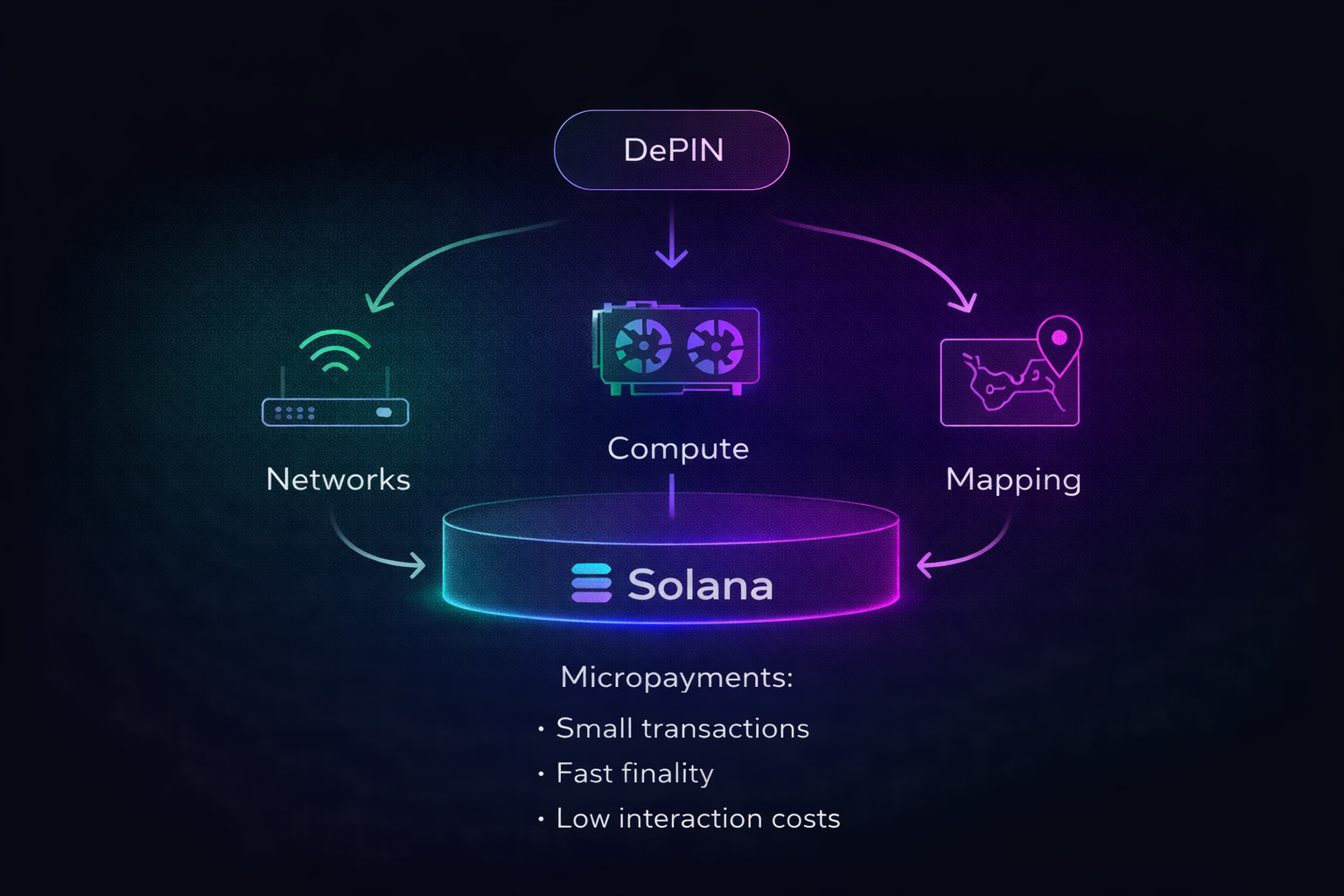

In parallel with the evolution of NFTs, Solana has emerged as one of the core layers for DePIN (Decentralized Physical Infrastructure Networks). Projects such as Helium, Render, and Hivemapper use Solana as their settlement and execution layer for real world physical infrastructure.

The primary reason DePIN projects choose Solana is micropayment economics. These networks require:

a large number of small transactions,

fast finality,

low interaction costs.

Solana satisfies these requirements without relying on complex off chain constructions or centralized workarounds. As a result, DePIN projects can directly tie economic incentives to physical activity, including data transmission, computation, and geolocation updates.

From an analytical perspective, the combination of state compression, NFTs as data assets, and DePIN forms one of Solana’s most important long term narratives. The network is gradually shifting from a purely financial layer toward an infrastructure for large scale digital and physical data flows, where economic activity is directly linked to real world usage.

It is precisely in this segment that Solana demonstrates a unique position. The network supports not only financial transactions, but also high frequency data flows. This opens the door to new categories of on chain products beyond traditional DeFi.

9. Payments, Stablecoins & Mobile UX

Solana’s payments narrative is a natural extension of its architectural priorities. While most L1s are optimized for storing or transferring large amounts of capital, Solana is designed for frequent, small, and fast transactions. These characteristics are critical for payments and consumer oriented use cases.

A key pillar of this direction is native USDC. On Solana, the stablecoin functions as a full featured on chain payment instrument:

with minimal fees,

near instant finality,

without the need for additional execution layers.

This makes Solana practical for scenarios where Ethereum or its L2s remain economically or UX inefficient, particularly for micropayments and recurring transactions.

Built on this foundation is Solana Pay, a payment protocol designed for direct peer to peer and merchant payments.

Its core value lies not in novel financial logic, but in reducing friction:

no intermediaries,

instant settlement finality,

transparent transactions.

Combined with stablecoins, this enables real world use cases in remittances, where speed and cost are decisive factors, especially in emerging markets. Importantly, these scenarios do not depend on high TVL or complex DeFi constructions. They are based on simple, repeatable utility.

A separate strategic pillar is Solana’s mobile first approach. Mobile devices are viewed not as a secondary interface, but as the primary access point to Web3. In this context, the launch of Saga was largely experimental, but it clearly signaled strategic intent. Control over the user experience at the device level.

This approach scaled through the Solana Mobile Stack, which includes:

secure on device key storage,

native dApp integration,

an alternative to centralized app stores without ecosystem taxes.

Strategically, this represents an attempt to remove one of the key bottlenecks to mass onboarding. Dependence on Web2 platforms that control application distribution and monetization.

Taken together, payments, stablecoins, and mobile UX form a clear positioning framework. Solana does not aim to become a universal settlement layer for global financial systems. Its objective is to serve as infrastructure for everyday transactions embedded within consumer products.

For this reason, Solana in this segment is conceptually closer to a Stripe like execution infrastructure than to a slow and expensive settlement layer. This does not diminish its financial role, but it clearly defines its focus. Mass adoption through simplicity, speed, and accessibility.

10. Governance, Devs & Institutions

Solana’s governance model differs significantly from the formalized on chain governance systems typical of many L1 networks. Solana lacks a rigidly structured governance framework, and this is not a design flaw but rather a reflection of its engineering and market philosophy.

In practice, network governance is shaped through a de facto balance of power rather than de jure voting mechanisms. The key participants in this process include:

core development teams,

validators,

protocols with substantial liquidity,

economically active users.

Decisions are driven less by formal proposals and more by coordination of interests, where economic viability plays a decisive role. This makes governance less transparent in the classical sense, but also more adaptive to rapid change and evolving technical requirements.

The developer layer plays a particularly important role in this system. Solana has one of the highest technical barriers to entry among major L1s:

a complex runtime architecture,

low level programming requirements,

high responsibility for resource optimization.

This limits the number of developers but simultaneously creates a quality filter. The ecosystem naturally favors teams capable of building high performance products rather than rapidly cloning existing solutions. Over the long term, this reduces fragmentation and raises the average level of technical maturity across projects.

After 2022, the gradual return of institutional participants became an important signal. Funds, market makers, and infrastructure players have re entered the ecosystem, but in a different form:

without a centralized backstop,

with greater focus on real usage metrics,

with a more cautious approach to risk.

As a result, institutional presence in Solana during 2024-2026 is more pragmatic and less narrative driven than in the previous cycle.

In summary, Solana’s governance model can be described as economically driven rather than procedural. It is less formalized, but closely tied to real network usage. For a consumer oriented execution layer, this is not a weakness but a logical continuation of the design philosophy. Fast decision making, technical focus, and minimal bureaucratic friction.

It is precisely this combination, a high technical barrier, an active developer community, and pragmatic institutional participation, that forms the social and governance foundation of Solana in the current cycle.

11. Competitive Landscape

Assessing Solana’s position requires comparison not at the level of abstract L1 vs L1 narratives, but through concrete architectural and UX trade offs that determine a network’s suitability for mass adoption.

The Ethereum L2 ecosystem currently dominates in terms of capital and institutional trust, but its key weakness remains user experience fragmentation. The proliferation of rollups results in:

fragmented liquidity,

complex onboarding,

reliance on bridges and abstraction layers.

For experienced users, these issues are partially manageable. For the mass consumer segment, however, this model remains overly complex. Ethereum L2s are optimized for settlement and scaling existing capital, not for fast and intuitive usage.

BNB Chain occupies a strong position in the utility segment and commands a large retail audience. Its primary advantage is deep integration with a centralized exchange and the broader Binance product ecosystem. At the same time, this is also its main limitation. Economic activity on BNB Chain is largely:

dependent on the exchange’s condition and strategy,

exposed to regulatory risk,

less organic in terms of independent on chain demand.

In this sense, BNB Chain is efficient but structurally dependent.

Tron remains an important player in payments and stablecoin transactions, particularly in certain regions. However, its development is characterized by:

limited innovation momentum,

low developer activity,

a narrow focus on a small set of use cases.

Tron is effective as a payments rail, but it does not cultivate an ecosystem capable of attracting new application categories.

Against this backdrop, Solana occupies a unique niche. It is:

monolithic by design,

scalable under real production loads,

optimized for high frequency execution without UX fragmentation.

Solana effectively remains the only L1 that combines high performance execution, cohesive UX, and scale without relying on external execution layers. This does not imply the absence of risks or trade offs, but it clearly defines its competitive identity.

From an analytical perspective, Solana does not compete directly with Ethereum as a settlement layer, nor does it replicate the BNB or Tron models. Instead, it occupies a distinct position. A high performance execution layer for consumer Web3, where the key metrics are speed, simplicity, and usage volumes rather than accumulated capital alone.

12. Risks

Despite Solana’s strong position in the current cycle, its investment and technological profile includes a number of structural risks that stem directly from its chosen architectural strategy. Ignoring these factors leads to a one sided assessment of the network.

Technical complexity

Solana is one of the most engineering intensive L1 networks. Its runtime, parallel execution model, and synchronization requirements create:

a higher likelihood of edge case failures,

greater difficulty in auditing and formal verification,

strong dependence on deep expertise within core development teams.

Unlike simpler execution models, Solana’s complexity does not scale linearly, which increases the risk of unexpected failures during peak usage.

History of downtime

In previous years, the network experienced partial and full outages. Although most of these issues have been addressed and overall stability has improved significantly, a reputational overhang remains. For users and institutions, downtime at the execution layer represents a critical risk, particularly in payment and high frequency use cases.

Hardware centralization

High infrastructure requirements:

increase capital expenditures,

reduce the pool of potential validators,

favor large operators and data centers.

This does not imply immediate centralization, but it creates structural pressure in that direction, requiring ongoing mitigation through economic and protocol level mechanisms.

Competition from Ethereum L2s

The Ethereum rollup ecosystem continues to evolve, reducing fees and improving UX through abstraction. If L2s succeed in:

significantly reducing fragmentation,

hiding complexity from end users,

preserving Ethereum’s economic advantages,

Solana’s competitive edge in the consumer segment could narrow.

Dependence on core development velocity

Solana relies heavily on:

the pace of core protocol development,

implementation of complex optimizations,

maintenance of client software and validator infrastructure.

Any slowdown in core dev velocity or internal coordination issues could have a disproportionate impact on network stability and competitiveness.

Taken together, these risks are not fatal, but they clearly define Solana’s trade off profile. The network offers scale and performance at the cost of increased complexity and operational risk. Both its growth potential and its limitations must be evaluated with these factors in mind over the medium and long term.

13. Growth Scenarios 2026-2028

Assessing Solana’s medium term potential requires a scenario based approach. Given the network’s strong dependence on real usage, the key variables are consumer adoption, infrastructure stability, and sustained narrative relevance. Below are three base scenarios for the 2026-2028 period.

Bull Case: consumer adoption as the dominant driver

In a positive scenario, Solana establishes itself as core infrastructure for consumer Web3. Mass adoption emerges at the intersection of:

payments and stablecoins,

DePIN with real economic flows,

high frequency on-chain activity (DeFi, memecoins, social applications).

Under these conditions, rising on-chain volumes translate into stable validator revenues, increased demand for SOL as both a gas and staking asset, and stronger network effects. Solana ceases to be viewed as an alternative and becomes one of the core execution layers of the crypto market, potentially allowing SOL to enter the top three assets by market relevance.

Base Case: dominance in the high volume segment

In the base scenario, Solana retains its current identity as a high performance network with large transaction volumes. Consumer adoption grows moderately, but the network:

remains a hub for retail activity,

dominates segments sensitive to fees and latency,

sustains a stable developer ecosystem.

In this case, Solana does not become a universal standard for all of Web3, but it maintains a durable competitive niche. SOL functions as an infrastructure asset with cyclical demand closely tied to on-chain activity.

Bear Case: technical or narrative breakdowns

The negative scenario materializes through a combination of:

serious technical failures or renewed downtime,

loss of trust among users and developers,

a narrative shift toward alternative execution solutions, primarily Ethereum L2s.

In this case, on-chain activity contracts, validator economics weaken, and Solana gradually loses its unique positioning. Importantly, the key trigger here is not competition per se, but a loss of internal development momentum.

Overall, the range of scenarios for Solana in 2026-2028 is wide but clearly defined. Its growth is not an automatic outcome of the market cycle. It depends directly on the network’s ability to maintain stability, scale real usage, and preserve its position as the most efficient execution layer for consumer Web3.

14. Conclusion

Solana should not be evaluated through the lens of classical narratives that have historically dominated assessments of blockchain assets. It is not digital gold, nor does it seek to function as a universal settlement layer for the global financial system. Such comparisons are methodologically flawed because they ignore Solana’s intended design and actual use cases.

Solana’s fundamental identity is that of a high speed execution layer optimized for mass usage in Web3. Its architecture, economics, and ecosystem are built around a single core objective: enabling fast, inexpensive, and scalable on-chain execution without fragmenting the user experience. This is precisely what makes Solana well suited for consumer applications where speed and simplicity are critical.

Within this framework, the primary growth driver for Solana is real usage. Not inflationary or deflationary mechanics, not artificial incentives, and not abstract metrics, but:

transaction volumes,

active user counts,

capital velocity,

the ability to sustain high frequency economic activity.

This is both a strength and a source of volatility. Solana excels in environments with strong demand for execution, but its economics are sensitive to declines in activity.

The key risk of this model is system complexity. High performance architecture requires:

rapid core protocol development,

stable infrastructure,

continuous management of technical trade offs.

Any disruption to this balance can have a disproportionate impact on trust and network usage.

Ultimately, Solana is neither a universal solution for all scenarios nor an ideological standard of decentralization. It is a specialized execution infrastructure focused on scale, speed, and mass market UX. Its long term value will be determined not by declarations, but by its ability to continue serving real demand in a consumer oriented Web3 environment.

Disclaimer:

This report is intended solely for informational and educational purposes and reflects independent commentary and analysis by the author. The author is not affiliated with any company mentioned in this report and holds no positions on the board of any related entities. All opinions, analyses, and insights expressed are the author’s alone and should not be interpreted as specific investment advice, a solicitation to buy or sell securities, or an endorsement of any particular investment strategy.The information provided is derived from sources and research the author deems reliable, but its accuracy, completeness, or timeliness is not guaranteed. Readers should not rely on this report as the sole basis for any financial decisions. The author disclaims any liability to update or revise the content as new information becomes available.

Investing involves significant risks, including the potential for loss of principal. Past performance does not guarantee future results. Investments or strategies discussed may not suit every individual’s circumstances, and they may fluctuate in price or value. This report does not consider your specific financial objectives, risk tolerance, or personal investment needs. Readers are encouraged to conduct their own research and consult with a qualified financial or investment advisor before making any investment decisions.

The author and any associated entities do not guarantee specific outcomes or profits from the use of this report. The author may or may not hold open positions in the securities mentioned. By reading this report, you acknowledge the risks involved and accept the limitations of the information presented.